None of the information provided is investment or tax advice. You should always read the associated risks before deciding whether to invest. These can be found on the product pages as well as in our risks overview. Please confirm you have read the information above.

The risk of capital loss is elevated—especially in overvalued mega-cap US stocks. But this does not foretell of an imminent crash. Instead, it’s a call to avoid overexposure to frothy areas.

Global trackers are heavily concentrated in expensive sectors, particularly AI-driven US equities. If history repeats (as in 2000), investors in these indices could face a decade of poor returns.

We remain fully invested but deliberately avoid overheated segments. Opportunities and lower valuation risk exist in areas like small caps and ex-US markets.

Downing launches new actively managed liquid alternatives fund aiming to deliver 7% to 10%+ per annum and positive returns in most markets. The new MGTS Downing Active Defined Return Assets Fund (‘Active Defined Returns’, the ‘Fund’), is the first fund from its new Liquid Alternatives team.

The Fund is aimed at institutional investors, Discretionary Fund Managers, IFAs and advised sophisticated individual investors, and will primarily consist of UK Government bonds and large-cap equity index options, which provide significant scalability and strong liquidity. It aims to deliver 7% to 10%+ per annum and positive returns in all markets except for a sustained equity market fall (generally more than 35%), over a period of at least six years.

The Fund is the first to be launched by the new Liquid Alternatives Team established by Downing. Collectively, the team has over 125 years of experience and sector knowledge, and includes Tony Stenning, who held senior roles at BlackRock and most recently was CEO of Atlantic House Group; Russell Catley, founder and also a former CEO of Atlantic House Group; Huw Price, a former Executive Director at Santander Asset Management, and Paul Adams, former Head of Cash Equities and Derivatives Sales, Royal Bank of Canada.

The Fund offers investors a compelling building block for multi-asset portfolios, aiming to add consistent and predictable returns, typically secured with a portfolio of UK Government bonds. The unique proposition includes a hybrid approach of using systematic derivative strategies and active management, combining liquid investments with predictable returns, and an equity like risk profile.

Investment strategy: Maximising the probability of delivering predictable defined returns across the economic cycle.

Systematic Liquid Derivatives: Systematic, derivative strategies optimise the equity risk-return profile. The Fund uses rules-based derivative strategies linked to the most liquid, large-cap global equity indices (i.e. FTSE100, S&P500) with the aim of harvesting well-proven consistent returns across a wide corridor of market conditions.

Strong security: The Fund will hold a high-quality portfolio of assets as secure collateral – typically UK Government bonds.

Active benefits: At times, rules-based, passive derivative strategies can underperform when markets move strongly – this is when specialist active management can add incremental gains by monitoring and monetising positions and applying active risk management.

Key benefits

Increased consistency and predictability of returns: Positive returns in all markets except for a sustained equity market fall of more than 35% over at least six years.

Diversification of risk: The Fund’s risk components are diversified across large, liquid equity indices, observation levels and counterparties. Secured with high-quality assets – typically UK Government bonds.

Active management: Our experienced team will actively manage the Fund and its investments to optimise risk and reward for investors.

Russell Catley, Head of Retail, Liquid Alternatives at Downing, said: “Put simply, we focus your investment risk on the probability of receiving the returns you need, not those you don’t. We target the highest probability of delivering 7% to 10%+ per annum with active management adding material incremental gains. We believe that we are building the next evolution of the proven success of Defined Returns funds

The Downing team isseeing strong demand from clients looking for alternatives to large-cap equity funds which are becoming concentrated in technology stocks, or alternatives to UK equity income funds and illiquid alternatives.”

Tony Stenning, Head of Liquid Alternatives at Downing, said: “The launch of our Active Defined Return Assets Fund is a significant milestone in the ambitious build-out of our new Liquid Alternatives strategies. It is a solution-focused fund that should deliver stable high single or low double-digit returns across a wide spectrum of equity market conditions, except for a persistent multi-year bear market. The Fund is designed to enhance balanced portfolios by providing consistent, predictable returns and is suitable for accumulation or drawdown.

“We aim to deliver a unique combination of proven systematic derivative strategies and specialist active management, and we are doing so at a very compelling fee level, below our closest competitors and in line with active ETFs.”

How the Fund is expected to perform in different markets

In bullish markets: UK Government bonds secure the capital, and the equity index options deliver a predictable 7-10%+ return per annum – giving up some less likely upside.

In neutral markets and normal market corrections: UK Government bonds secure the capital, and the index options deliver a predictable 7-10%+ return per annum.

In a sustained sell-off: if markets fall more than the cover to capital loss and do not recover for six years. Then capital is eroded 1:1 in line with the worst performing index.

The average Cover to Capital Loss is targeted at 35%: the average cover to capital loss represents the average level the Global indices within the Fund could fall before capital is at risk.

Fund key risks

Performance: Capital is at risk. Investors may not get back the full amount invested.

Liquidity: Access to capital is always subject to liquidity.

Counterparty risk: Other parties could default on the contractual obligations.

Fund Structure

UK regulated OEIC fund structure, fully UCITS compliant

Daily dealing, at published NAV

Minimum investment: £100,000

SRRI: 6 out of 7

Depositary: Bank of New York

Authorised corporate Director (‘ACD’): Margetts Fund Management Ltd.

I share-class: SEDOL: BM8J604 / ISIN: GB00BM8J6044

F share-class: SEDOL: BM8J615 / ISIN: GB00BM8J6150

Risk warning: Opinions expressed represent the views of the fund manager at the time of publication, are subject to change, and should not be interpreted as investment advice. Please refer to the latest full Prospectus and KIID before investing; your attention is drawn to the risk, fees and taxation factors contained therein. Please note that past performance is not a reliable indicator of future results. Capital is at risk. Investments and the income derived from them can fall as well as rise and investors may not get back the full amount invested. Investments in this fund should be held for the long term.

Important notice: This document is intended for professional investors and has been approved as a financial promotion in line with Section 21 of the FSMA by Downing LLP (“Downing”). This document is for information only and does not form part of a direct offer or invitation to purchase, subscribe for or dispose of securities and no reliance should be placed on it. Downing does not offer investment or tax advice or make recommendations regarding investments. Downing is a trading name of Downing LLP. Downing LLP is authorised and regulated by the Financial Conduct Authority (Firm Reference No. 545025). Registered in England and Wales (No. OC341575). Registered Office: 10 Lower Thames Street, London EC3R 6AF.

Is the market about to crash?

From my recent conversations with you, I gather some of your clients are worried that the stock market’s about to crash. So, let’s get into that.

Regular readers know what’s coming next (ironic, as it’s a warning that nobody can know what’s coming next). Yes; it’s our usual caveat that we don’t know what the future holds.

Predicting markets is even harder than predicting weather. Weather forecasts are notoriously imperfect, but at least they’re improving (although they still quickly degrade as you move away from now). Market forecasters, in contrast, are still no better than that ancient Cornish sea dog muttering ‘aye, there’s a storm a-brewing’ from his corner of the pub. Should you happen to be in The Anchor and Sprat as he issues his warning and are later hit by an unexpectedly savage tempest, you’ll think him supernaturally wise. Until, that is, you speak to the pub’s landlord, who tells you he’s said the same thing every day for the last ten years.

This is why we don’t make predictions: We know they’re likely to be wrong but, once made, it’s hard not to let them influence your actions. However, I get that this is a killjoy attitude. Having a go at reading the markets’ tea leaves is fun so, for once, I will suspend my po-faced reluctance and join in (but I’ll be clear; none of this will impact how the Fox Funds are managed).

Reading the Runes

Firstly, let’s separate risks from predictions. I think the risk of serious capital loss from investing in the market is currently high (see last quarter’s letter here). But that’s different to saying the market’s about to crash. It’s also different to saying that everything in the market is risky. Because it’s entirely possible that, even if the market index does take a swan dive, there will be companies and sectors within the market that don’t.

My concern stems from high valuations in certain areas, with mega-cap US growth stocks central to that. And as these now make up a massive part of the global market, you can extend my concern to the market cap-weighted index that’s tracked by passive products (and closet tracked by many more supposedly active ones).

But while valuations indicate that losses from a crash may be severe, they don’t tell you when, or even if a crash will happen. Never have, never will.

What does?

Not much. But if I were to rely on anything – and it’s now that I light my pipe and don my anchor-motif cap – it’s reading the public mood. In the past I’ve called this looking for ‘cabbieflags’, which I explained in my letter from August last year:

“When people ask me if the recent AI bubble has started to burst, what stops me saying anything more certain than ‘I hope so’ is that too many industry outsiders are as yet insufficiently amazed/terrified about what AI can do. It’s the absence of this cabbieflag (the warning provided by a taxi driver when he says you’d be mad not to invest in the latest big thing) that makes me think there’s a puff or two yet to be blown into this particular balloon.” Q3 2024 Fox Investment Letter

That has proved disappointingly true. Disappointing, because the bigger this balloon gets, the more painful any deflation will be.

What has changed since then is the public mood. Firstly, many more people now ‘get’ AI and how it will change the world. Secondly, from what I’ve seen, more individuals are rushing to either buy into the theme or into the market trackers that are heavily exposed to it1.

So, the cabbieflags are fluttering, but are we near a peak? My gut still says there’s a way to go, but it does at least feel like we’re entering the final stage. In past cycles, the final stages were marked by frenzied retail investors buying shares from institutional holders (who were tiptoeing towards the exits), and that’s beginning to happen again today.

So maybe we’re within, say, 18 months of a peak. Getting more precise than that requires deeper stroking of the ancient-mariner beard. So here goes: I feel a sell-off is more likely in spring or autumn, so if you make it through November unscathed you may be able to relax for a few months as Santa delivers his usual (but not guaranteed) rally. Then you’re into Ides-of-March territory when, if I was deep into this particular trade, I’d begin to get a little sweaty. Many a bull market has died just as the daffs are blooming.

Enough with the ridiculous

Of course, this is all ludicrous (but I enjoyed it anyway). It’s superstition and hope, neither of which are good strategies. My 18-month call could be wrong in so many different ways: The market might crash tomorrow; it might drag on another five years; or I might be right about the peak, but it gently deflates instead of crashing; or maybe we’ve entered a new historical paradigm and the current trend goes on forever.

Perpetually trying to forecast this stuff could drive you mad. Which is why I don’t (I’m a middle-aged parent - there are enough things exasperating me as it is). What do I do instead?

I prefer to prepare, not predict. I said above I’d be worried if I was deep into this particular trade. Well, therein lies the answer: If it worries you, don’t get deep into this particular trade.

Happily, it doesn’t have to be an ‘in’ or ‘out’ question, there’s a third option: ‘in, but in different stuff’. Because markets are currently polarised. Some parts - most obviously US mega caps - look worryingly expensive. But just about everything else ranges from ‘fine’ to ‘once-in-a-generation cheap’ (many small-cap markets, for example).

In fact, despite all the worries about market craziness, it's really not hard to find great opportunities. But ‘find’ is the key word here. Because you will need to actively find these opportunities, as you can’t rely on a classic market tracker doing it for you. These have become highly concentrated in both US equities and mega-cap companies, and that’s not about to change (not in a painless way, anyway):

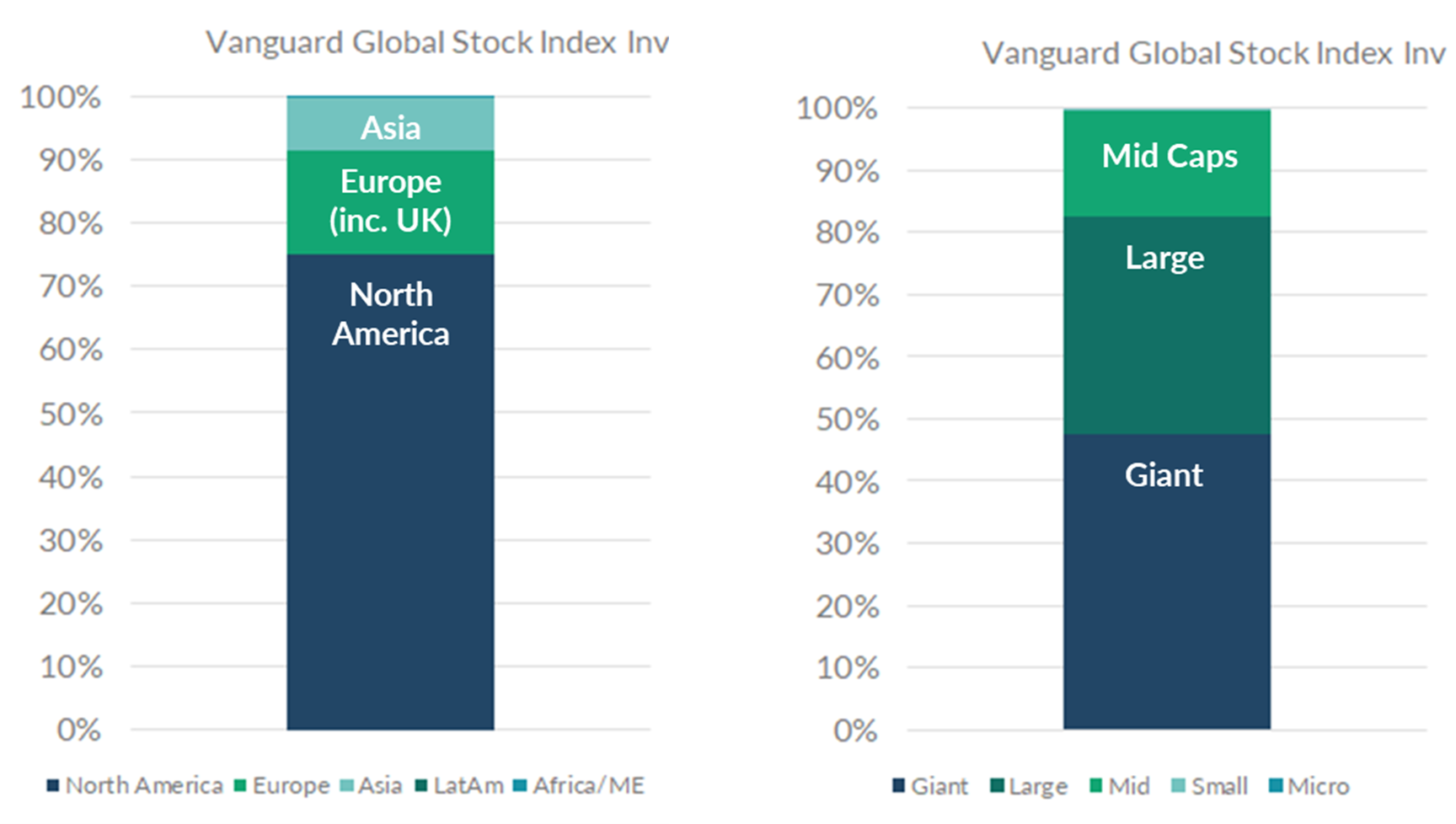

Exposures within the Global Index Tracker

Source: Morningstar, as at 31.07.2025

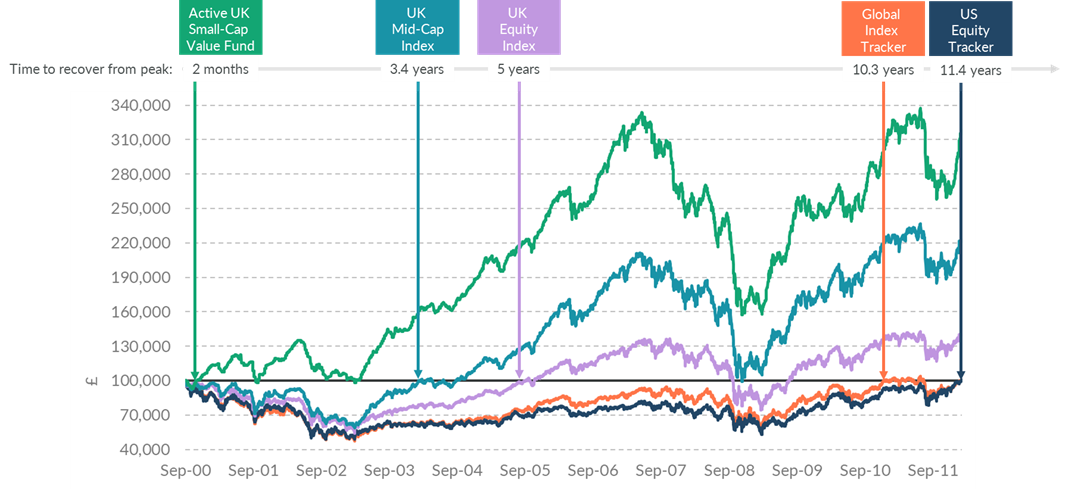

As the following chart from the noughties shows; the global market doesn’t have a god-given right to keep rising, particularly when its largest geographical component is falling through the floor. Back in 2000, the proceeding decade of global index woes were driven by the US market’s dramatic reversal, at a time – take note - when American shares were ‘only’ 50% of the global tracker, not the 70%+ they are today.

Past performance is not an indication of future performance. Source: Morningstar and Downing Fund Managers. Total Return, in GBP terms. 14.09.2000 to 14.02.2012 Components are: Aberforth UK Small Companies Acc; FTSE 250 Index; FTSE All-Share Index; Vanguard Global Stock Index USD Acc & the Vanguard 500 Index Investor.

Just take a moment to consider this. Market conditions look a lot like they did in 2000. Should history repeat itself, anyone fully invested in the global tracker - or anything like it - will go ten years without making money. No client, least of all one who’s around retirement age, will thank you for that.

It’s not just passive products though. Think back to 2022 and the obvious risks that had built up in bond markets. Yet many (most?) ‘active’ asset allocation strategies were still heavily invested in bonds, as they weren’t prepared to separate from the herd. This is closet tracking at a macro level: Too many were paying lip service to the risks, not avoiding them. I believe the same trip hazard is there today, only this time it’s equities rather than bonds.

What’s the rub?

OK; Staying invested, but avoiding the dangerous bits sounds obvious, right? Surely there has to be a cost?

Yes, there is: Avoiding hot areas means looking slow while they heat up.

I’m personally fine with this. A bubble, like binge drinking, is a young person’s game – fun but ultimately ill-advised, and the older you are, the harder the recovery.

In this sense, staying invested but avoiding the bubbly stuff is like playing ‘walking football’. This is a slowed-down version of the game (predominantly played by over 50s), which gives you some of the enjoyment and exercise of the full-blooded version, albeit with less exhilaration. The upside? You’re less likely to break a hip.

And this is how it’s been at Downing Fox. The funds are 28 months’ old, and our 100% equity fund has made 28%2. This is a decent clip, but it’s considerably less than you’d have got from a global tracker. But we’re playing different games. It’s been a raging AI-driven bull market, and the global tracker has been highly exposed to that, but we haven’t (we’re stubbornly diversified). So there’s your trade-off: Financially speaking we’re jogging, not sprinting, but I think we’re less likely to end up in traction3.

But isn’t it different this time?

Another comment I’m hearing is that it’s different to 2000, as back then it was frothy, non-profit-making companies that caused the harm. Is this true?

I don’t think so. Yes, the companies at the top of the market are among the best and most profitable companies we’ve ever seen. They’re certainly far from being Pets.com, which was the poster child for late-nineties excess (it IPO’d in February 2000, immediately crashed, and was bust nine months later).

But at a market level, spectacular-but-small flame outs like that weren’t the problem. Even Amazon’s (temporary) 94% crash4 (ninety four!) played a relatively minor role, as it was a far smaller part of the index back then. Instead, it was the likes of Microsoft – the world’s biggest company in 2000 - dropping by 65%5 that dented index-level returns.

It doesn’t matter how good a company is if its share price is too expensive. From there it’s destined for disappointment (at best). Take Cisco, the market’s second-biggest constituent in 2000. This is a great company that has – as predicted back in 1999 - made massive profits from the rise of the internet. You could have made a bundle from buying its shares, but not if you bought at its 2000 peak (you’d have made 1.1% a year for 25 years, less than both cash and inflation). Or, for that matter, if you bought it when the bubble was only half-way inflated (a 3.6% annualised return is flaccid given the rollercoaster journey it put you through6).

Past performance is not an indication of future performance. Source: Morningstar Direct, annualised USD terms, 17.02.1990 to 30.09.2025. Then: 27.03.1998; 16.11.1999; 27.03.2000; 11.10.2002; and 14.08.2011 all to 30.09.2025.

Are today’s biggest companies at a similar point of overvaluation? I’m not the person to answer that, as I don’t analyse stocks. But I think you’d be crazy to not at least acknowledge the risk that they might be and adjust your exposure accordingly. You simply don’t need to be ‘all in’ on this.

The Wrap Up

I’m a great believer in the old adage that it’s time in the market that matters, not timing the market. This is why I created Downing Fox – I want to stay invested in equities to benefit from the extraordinary benefits of compounding, but I honestly don’t think I could stay invested in ‘the market’ (as defined by MSCI) as it stands today. It’s simply too concentrated in a handful of potentially risky shares, and much as I don’t know if or when it may crash, the fact that itmight is enough for me. But a portfolio of market-listed companies selected by independent, valuation-conscious expert investors? There’s no good reason to sell out of that today. Which is why I haven’t.

1 I’ve seen a fair bit of retail fervour in the UK, but what matters more is the man or woman on the average American street. Our recent conversations with our US-based managers suggest the mood over there is a degree or two hotter than the cooler-blooded British equivalent. 2 The MGTS Downing Fox 100% Equity A Shares made 27.6% between launch on 27.06.2023 and 27.10.2025, after charges. Source: FE Analytics. Past performance is not a reliable indicator of future performance. 3 To be clear, it’s highly unlikely that, should the markets’ giants tumble, the stocks we own will avoid all the turbulence. But I firmly believe that if we – and our chosen managers – do our job properly, any equity falls we see should be shorter and shallower than the index’s. 4 Source Morningstar Direct, USD terms, 13.12.1999 to 29.09.2001. 5 Source Morningstar Direct, USD terms, 31.12.1999 to 20.12.2000. 6 And let’s be honest, unless you misplaced the certificates or forgot you owned it, you didn’t hang on to these shares on account of the painful experience.

Opinions expressed represent the views of the fund manager at the time of publication, are subject to change, and should not be interpreted as investment advice.

Important notice: this document has been prepared for professional investors and has been approved as a financial promotion by Downing LLP (“Downing”). Capital is at risk and investors should note that their investments and the income derived from them can fall as well as rise and investors may not get back the full amount invested. Downing does not offer investment or tax advice or make recommendations regarding investments. Downing is a trading name of Downing LLP. Downing LLP is authorised and regulated by the Financial Conduct Authority (Firm Reference No. 545025). Registered in England and Wales (No. OC341575). Registered Office: 10 Lower Thames Street London EC3R 6AF.

.jpeg)

.png)