None of the information provided is investment or tax advice. You should always read the associated risks before deciding whether to invest. These can be found on the product pages as well as in our risks overview. Please confirm you have read the information above.

The ‘do-nothing model’ of investing - typically a passive, autopilot approach using global index trackers - has delivered excellent returns with minimal effort or cost.

However, this model may be heading for trouble due to overexposure to US equities and historically high valuations.

The do-nothing model won’t adapt to changing risks on its own, so advisers might consider reviewing their CIP to check for potential problems.

Downing launches new actively managed liquid alternatives fund aiming to deliver 7% to 10%+ per annum and positive returns in most markets. The new MGTS Downing Active Defined Return Assets Fund (‘Active Defined Returns’, the ‘Fund’), is the first fund from its new Liquid Alternatives team.

The Fund is aimed at institutional investors, Discretionary Fund Managers, IFAs and advised sophisticated individual investors, and will primarily consist of UK Government bonds and large-cap equity index options, which provide significant scalability and strong liquidity. It aims to deliver 7% to 10%+ per annum and positive returns in all markets except for a sustained equity market fall (generally more than 35%), over a period of at least six years.

The Fund is the first to be launched by the new Liquid Alternatives Team established by Downing. Collectively, the team has over 125 years of experience and sector knowledge, and includes Tony Stenning, who held senior roles at BlackRock and most recently was CEO of Atlantic House Group; Russell Catley, founder and also a former CEO of Atlantic House Group; Huw Price, a former Executive Director at Santander Asset Management, and Paul Adams, former Head of Cash Equities and Derivatives Sales, Royal Bank of Canada.

The Fund offers investors a compelling building block for multi-asset portfolios, aiming to add consistent and predictable returns, typically secured with a portfolio of UK Government bonds. The unique proposition includes a hybrid approach of using systematic derivative strategies and active management, combining liquid investments with predictable returns, and an equity like risk profile.

Investment strategy: Maximising the probability of delivering predictable defined returns across the economic cycle.

Systematic Liquid Derivatives: Systematic, derivative strategies optimise the equity risk-return profile. The Fund uses rules-based derivative strategies linked to the most liquid, large-cap global equity indices (i.e. FTSE100, S&P500) with the aim of harvesting well-proven consistent returns across a wide corridor of market conditions.

Strong security: The Fund will hold a high-quality portfolio of assets as secure collateral – typically UK Government bonds.

Active benefits: At times, rules-based, passive derivative strategies can underperform when markets move strongly – this is when specialist active management can add incremental gains by monitoring and monetising positions and applying active risk management.

Key benefits

Increased consistency and predictability of returns: Positive returns in all markets except for a sustained equity market fall of more than 35% over at least six years.

Diversification of risk: The Fund’s risk components are diversified across large, liquid equity indices, observation levels and counterparties. Secured with high-quality assets – typically UK Government bonds.

Active management: Our experienced team will actively manage the Fund and its investments to optimise risk and reward for investors.

Russell Catley, Head of Retail, Liquid Alternatives at Downing, said: “Put simply, we focus your investment risk on the probability of receiving the returns you need, not those you don’t. We target the highest probability of delivering 7% to 10%+ per annum with active management adding material incremental gains. We believe that we are building the next evolution of the proven success of Defined Returns funds

The Downing team isseeing strong demand from clients looking for alternatives to large-cap equity funds which are becoming concentrated in technology stocks, or alternatives to UK equity income funds and illiquid alternatives.”

Tony Stenning, Head of Liquid Alternatives at Downing, said: “The launch of our Active Defined Return Assets Fund is a significant milestone in the ambitious build-out of our new Liquid Alternatives strategies. It is a solution-focused fund that should deliver stable high single or low double-digit returns across a wide spectrum of equity market conditions, except for a persistent multi-year bear market. The Fund is designed to enhance balanced portfolios by providing consistent, predictable returns and is suitable for accumulation or drawdown.

“We aim to deliver a unique combination of proven systematic derivative strategies and specialist active management, and we are doing so at a very compelling fee level, below our closest competitors and in line with active ETFs.”

How the Fund is expected to perform in different markets

In bullish markets: UK Government bonds secure the capital, and the equity index options deliver a predictable 7-10%+ return per annum – giving up some less likely upside.

In neutral markets and normal market corrections: UK Government bonds secure the capital, and the index options deliver a predictable 7-10%+ return per annum.

In a sustained sell-off: if markets fall more than the cover to capital loss and do not recover for six years. Then capital is eroded 1:1 in line with the worst performing index.

The average Cover to Capital Loss is targeted at 35%: the average cover to capital loss represents the average level the Global indices within the Fund could fall before capital is at risk.

Fund key risks

Performance: Capital is at risk. Investors may not get back the full amount invested.

Liquidity: Access to capital is always subject to liquidity.

Counterparty risk: Other parties could default on the contractual obligations.

Fund Structure

UK regulated OEIC fund structure, fully UCITS compliant

Daily dealing, at published NAV

Minimum investment: £100,000

SRRI: 6 out of 7

Depositary: Bank of New York

Authorised corporate Director (‘ACD’): Margetts Fund Management Ltd.

I share-class: SEDOL: BM8J604 / ISIN: GB00BM8J6044

F share-class: SEDOL: BM8J615 / ISIN: GB00BM8J6150

Risk warning: Opinions expressed represent the views of the fund manager at the time of publication, are subject to change, and should not be interpreted as investment advice. Please refer to the latest full Prospectus and KIID before investing; your attention is drawn to the risk, fees and taxation factors contained therein. Please note that past performance is not a reliable indicator of future results. Capital is at risk. Investments and the income derived from them can fall as well as rise and investors may not get back the full amount invested. Investments in this fund should be held for the long term.

Important notice: This document is intended for professional investors and has been approved as a financial promotion in line with Section 21 of the FSMA by Downing LLP (“Downing”). This document is for information only and does not form part of a direct offer or invitation to purchase, subscribe for or dispose of securities and no reliance should be placed on it. Downing does not offer investment or tax advice or make recommendations regarding investments. Downing is a trading name of Downing LLP. Downing LLP is authorised and regulated by the Financial Conduct Authority (Firm Reference No. 545025). Registered in England and Wales (No. OC341575). Registered Office: 10 Lower Thames Street, London EC3R 6AF.

End of the road for the do-nothing investment model?

There’s an investment proposition favoured by many advisers I’d call the ‘do-nothing model’. Having worked brilliantly for a long time, it’s become highly popular: Good returns; smooth journey; low hassle; and cheap as chips. What’s not to like about that? The trouble is it might be about to drive itself into a brick wall.

What do I mean by the ‘do-nothing model’?

It’s the advice model where, once an adviser has risk-profiled a client, no further investment decisions are made on that client's behalf. The choice between sub-asset classes? Geographical split? Individual shares? All set by pre-defined criteria, then left to run on autopilot.

In other words, all the investment decision makers have been removed (which helps to explain why it’s so cheap). Given the chequered history of decision makers in the investment world, I can understand how this might seem a good thing.

That’s not all though. A further advantage is that the decision-free model is useful for regulatory and legal purposes: If no one in the chain between the client and the market has made an investment decision (i.e. they’re just efficiently doing what they said they would, but no more than that), then no party can be blamed if the investments go wrong.

It's what’s known as an ‘accountability sink’: A tangled web of committees, regulations, disempowered employees, helpless customers, outsourced responsibilities and legal back covering.

Accountability sinks tend to function well enough for a while, causing little more than low-level frustration as they expand, but one day they implode. And when they do? There’s no individual to take responsibility – just a circle of fingers pointing at someone else1. (It’s not just a financial services phenomenon by the way, they’re appearing across our society: The Grenfell Tower fire was a particularly tragic example.)

That’s the ‘do-nothing’ investment model in principle. What does it contain in practice?

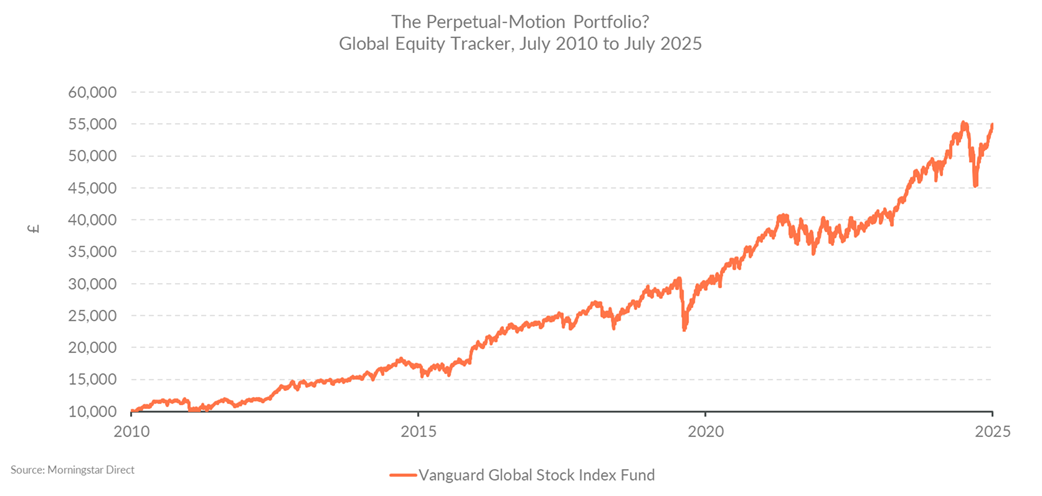

This is the engine that currently powers it: The global stock market.

Past performance is not an indication of future performance. Source: Morningstar and Downing Fund Managers. Total Return, in GBP terms. 31.07.2010 to 31.07.2025

In this instance, it’s represented by Vanguard’s global index tracker fund. Vanguard is an outstanding organisation. There are few companies on the planet as good at setting out what it’s going to do, then reliably doing it. That’s what this fund does: Vanguard promises it will track the global stock market efficiently and cheaply. And it tracks the global stock market efficiently and cheaply. I have nothing but admiration for the firm and its business model (we use its products ourselves2).

What Vanguard doesn’t do is change what’s in its global tracker if that becomes worrying in some way. They’re very clear about this. It means they don’t make mistakes – they just carry on doing what they promised they’d do. And if what’s inside the index goes wrong? That’s on you. Their job is simply to track that index - for better or for worse. In other words; this letter is many things, but it’s not a pop at Vanguard.

As you can see from the chart, this has worked superbly. Be you adviser or private investor, that one decision – to buy a global tracker then leave it alone - has made you 12% a year for 15 years: Sweet. It’s worked so well, and for so long, that many more individuals, advisers, and investment committees are tuning into it. It’s become a default: Switch to the global model - or some minor variation of it - and you’ll receive a reliable stream of great returns. And if it goes wrong? Don’t worry! It’s not your fault – you were only doing what you said you would.

Here's the rub: Nothing in markets works forever. If something has produced uncommonly high returns for an uncommonly long time, there’s a high chance it borrowed some of those returns from the future. Unfortunately, financial gravity will eventually kick in, and it will have to pay those back. Usually this is by producing uncommonly low (or negative) returns for an uncommonly time (or, worse, going bust – but I don’t think that’s on the cards here).

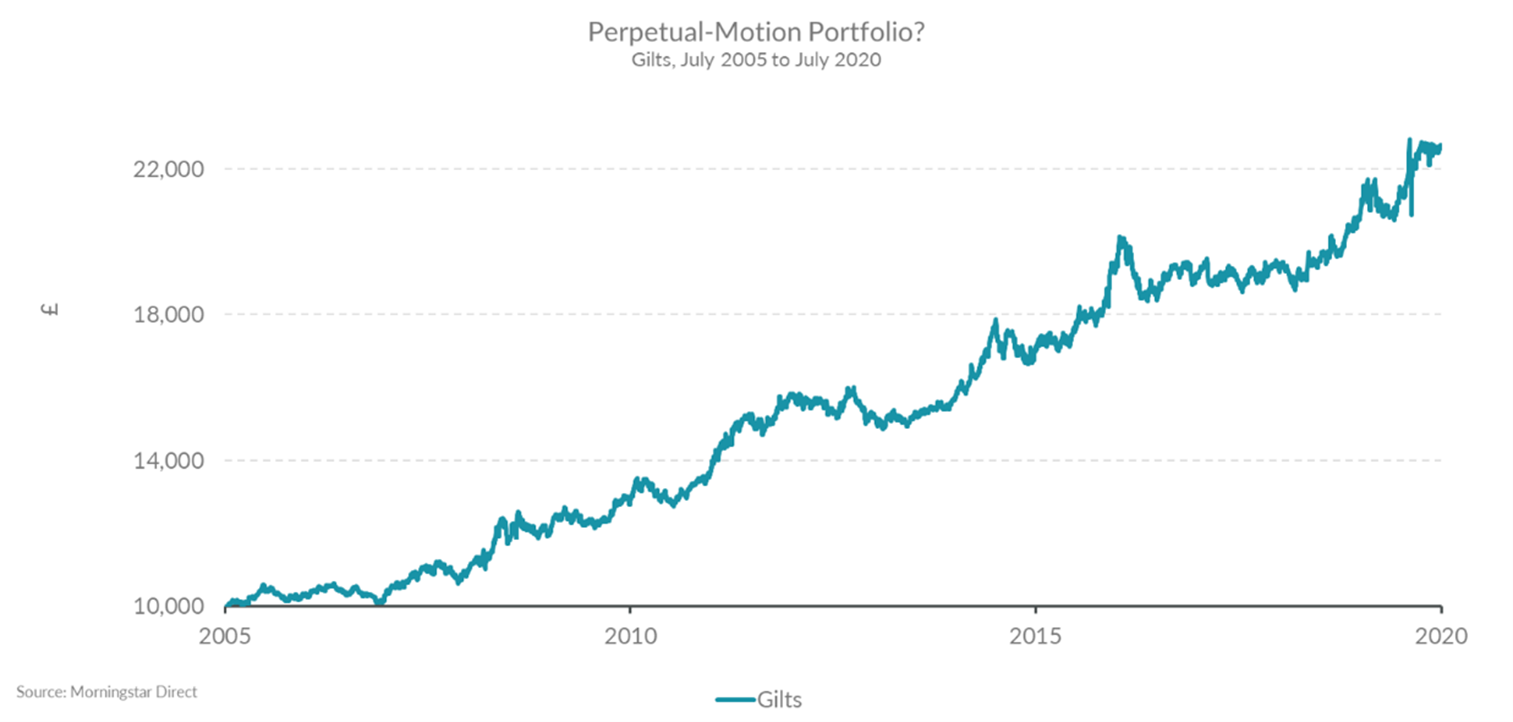

It’s not hard to find historical examples. In fact, we only need to look back a few years to see the last time a do-nothing investment model reversed. Step forward the bond market, which – five years ago - looked like this in the rearview mirror:

Past performance is not an indication of future performance. Source: Morningstar and Downing Fund Managers. FTSE Actuarial UK Conventional Gilts All-Stocks Index. Total Return, in GBP terms. 31.07.2005 to 31.07.2025

Why wouldn’t you set and forget that into your multi-asset portfolio?

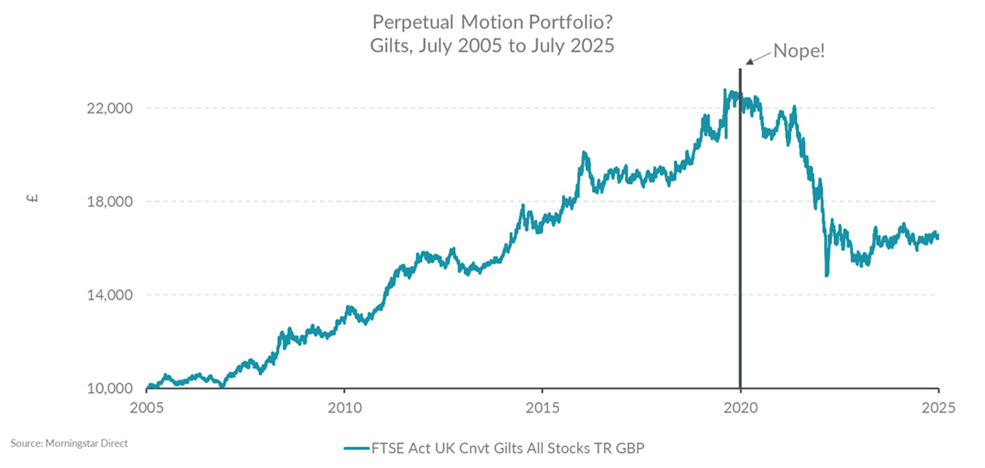

The reason, it turns out, was because inflation had been uncommonly low for an uncommonly long time. This meant gilts (and most other bonds) had over-earned, making them dangerously expensive. When inflation returned (most notably in 2022), they instead began paying an uncommonly low amount for an uncommonly long time (five years and counting, so far):

Past performance is not an indication of future performance. Source: Morningstar and Downing Fund Managers. FTSE Actuarial UK Conventional Gilts All-Stocks Index. Total Return, in GBP terms. 31.07.2005 to 31.07.2025

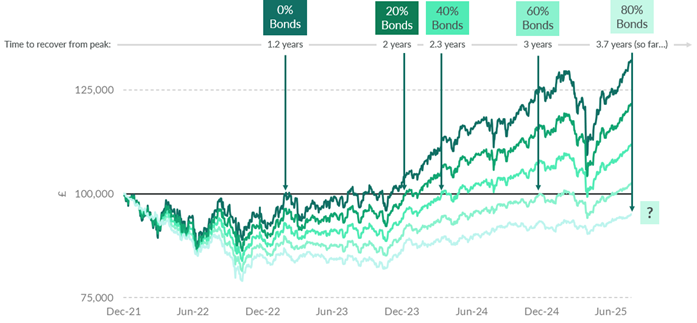

What happened if you did set and forget a no-decision bond exposure into your multi-asset portfolio? The chart below shows the impact within a set-and-forget fund range with passive exposure to a pre-set selection of bond trackers:

Past performance is not an indication of future performance. Source: Morningstar and Downing Fund Managers. Total Return, in GBP terms. 08.12.2021 to 31.07.2025 Components are the A Accumulation share classes of the five funds within a popular passive multi-asset fund range.

It wasn’t pretty: The more bonds you held, the bigger – and longer - your losses. And, because it’s typically the most risk-averse investors who hold the most bonds, this was a particularly damaging outcome.

Why didn’t somebody do something?! Is a question much asked since then. Wasn’t it obvious bonds were dangerous? Well, yes, it was. It was an open industry secret that bonds had become all risk and no return, and yet still clients were autopiloted into the abyss. This is a marker of an accountability sink – plenty of insiders know it’s wrong, but nobody seems willing or able to fix it.

Anyway, that was bonds, and this is about equities; the other part of a multi-asset portfolio. The question is, can the same thing happen to them?

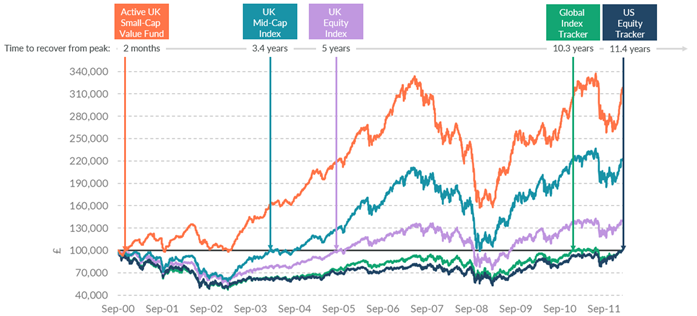

Yes; I think it can. Helpfully, there’s a precedent for this too. Because while the last 15 years has been all sunshine and roses for the global equity tracker, the ten years before that was a barren wasteland:

Past performance is not an indication of future performance. Source: Morningstar and Downing Fund Managers. Total Return, in GBP terms. 14.09.2000 to 14.02.2012 Components are: Aberforth UK Small Companies Acc; FTSE 250 Index; FTSE All-Share Index; Vanguard Global Stock Index USD Acc & the Vanguard 500 Index Investor.

Hence why it’s not outrageous to suggest that something as apparently reliable as a global tracker could go a long time without making money. Because that’s exactly what it did between September 2000 and December 2010. Ten years: Nothing. Imagine explaining that to your clients.

Next question then; how likely is it that this could happen again today?

Back in 2000, the problem was that the global tracker had become heavily concentrated in US equities, and US equities had over-earned in the prior 15 years, making them dangerously expensive. The result? When the American stock market corrected, it dragged the global tracker down lower and for longer than if it had contained no US exposure (UK equities, for example took less than half the time to recover their previous peak – see chart).

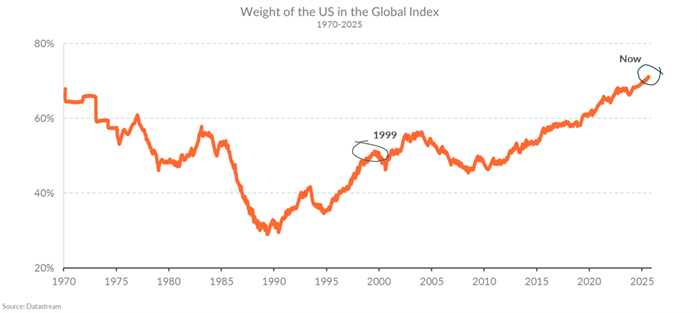

Let’s compare and contrast those factors with today, starting with US equity concentration: How much of the global tracker is held in American shares today compared to 2000?

Past performance is not an indication of future performance. Source: Downing Fund Managers & Datastream / Albert Edwards, Societe Generale, Economist & Global Strategist, Data 1970 to 2025.

That’s not a good start. In 2000 the global index was around 50% exposed to US equities, today it’s over 70%. So, if the US does have a rougher ride than other global markets, it will have a bigger negative impact than it did in the 00s.

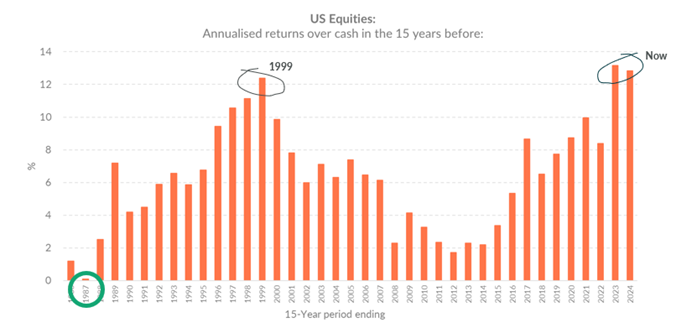

Next up; have US equities over-earned in the last 15 years?

Clearly this is subjective, but again the pattern doesn’t look good:

Past performance is not an indication of future performance. Source: Morningstar and Downing Fund Managers. Total Return, Rolling 15-Year periods, S&P 500 annualized return less annualised returns of the Federal Funds rate. 01.01.1986 to 31.12.2024.

The last 15 years has been an exceptionally good run for US equities; matched only by the 15 years ending in 1999. Only hindsight will tell us if they’ve over-earned again, but it certainly doesn’t look like we’ve been underpaid for holding them.

By the way, that green circle over 1987? That’s the worst 15-year period my data covered, and it began in 1972. If you check the chart prior to this one, you’ll see 1972 was the last time global markets were this concentrated in US equities. This is another worrying precedent.

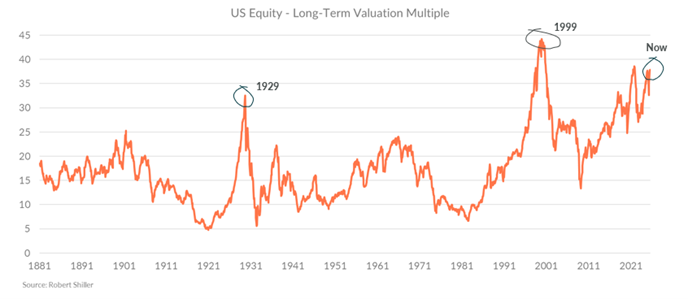

Finally, let’s compare today’s valuations of US equities to 2000. Here we find better news (at last!). US equities are cheaper today than they were in 1999:

Past performance is not an indication of future performance. Source: Downing Fund Managers & Robert J Shiller, CAPE Ratio, January 1881 to August 2025.

Sadly, ‘cheaper’ doesn’t mean ‘cheap’. On this widely respected measure, 1999 is the only time in 144 years that US shares have been more expensive than they are today. And that includes the peak just before the Great Wall Street Crash of 1929, which heralded the Great Depression.

All in all, it doesn’t look good. Considering this, I think a better question than ‘will it happen?’ is ‘why wouldn’t it happen?’

Potential answers to that include:

• Because there’s a technological revolution happening, and the US is at the centre of it.

• Because American companies are better than non-American companies.

• Because large companies (which dominate the index, and like 2000 are more richly valued than smaller companies), are better than smaller companies.

• Because passive investing has become too big to fail. So, if it does happen again, this time governments and central banks will step in to prevent it.

The first three points are exactly what investors were saying at the start of 2000, so I’d take these with a pinch of salt. But the fourth one? This is the one that troubles me. It’s certainly in our leaders’ characters to try to stop this from happening, perhaps by printing money to buy the US equity index. Heaven only knows what that would mean for the real world though (‘Death of Capitalism!’ headlines wouldn’t seem a stretch in that scenario).

Which brings me to my usual caveat, which is that I’m highlighting all of this as a risk, not a stick-on prediction. Maybe something is different this time, and staying with the global tracker - or something like it - will continue to be the best way to go. But with all these concerns buzzing around my head, I’d feel bad if I didn’t at least point out how big a risk I think this is, and how likely I feel it may be. I hope that, if nothing else, it’s food for thought.

The other thing to say is that much as this all seems very doomy and gloomy, it needn’t be. This chart, taken from the excellent work done by Research Affiliates, suggests that – once you get away from US mega caps - there’s no shortage of reasonably valued markets that look set for a perfectly good decade:

Expected 10-Year real returns based on Research Affiliates’ estimates:

Estimated forecasts are not a guaranteed indicator of future performance. Source: Research Affiliates as at August 2025. Note: Research Affiliates’ interactive tool uses historical data to generate estimate outcomes that are hypothetical in nature and does not recommend securities. Results may vary with each use and over time.

A cynic might suggest I'm saying this to pimp Downing Fox’s equity portfolio as an alternative to a global tracker. And that cynic is probably right: Like a global tracker, it holds loads of companies. But because it only holds actively managed funds, it naturally adapts itself to changes in valuation and quality of the c.1,000+ companies it holds. This is exactly what I designed it for; to provide investors with the diversification of a tracker (or the diversification a tracker used to provide, anyway), but to constantly move itself away from build-ups of risk and towards opportunity. This adaptability is why I’m comfortable being all in on it with my own money. But yes; it’s far from the only alternative. In fact, you don’t even need to buy active funds: Vanguard themselves offer plenty of reliable ways of passively accessing these markets, thereby reducing the risks I've set out here.

That will, however, mean someone, somewhere making some decisions. Because the do-nothing model won’t do it for you. So, here’s the final question: When it comes to your own investment model, is there someone making that call for your clients? Or is it on autopilot?

1 To be clear; I don’t mean to throw shade on advisers operating this model. There’s usually no willfully bad intent from any members of an accountability sink, often they’re powerless to the system. Such sinks form like tornadoes – natural phenomena resulting from a particular mix of climatic conditions, and participants often have little choice but to join in. If you’d like to know more, I’d recommend Dan Davies’ excellent book ‘The Unaccountability Machine’.

2 We hold some of Vanguard’s government bond trackers in the non-equity parts of our multi-asset funds. And in the past we’ve also held one of its active funds in our equity portfolio too (they are a huge active fund manager, in case you didn’t know).

Opinions expressed represent the views of the fund manager at the time of publication, are subject to change, and should not be interpreted as investment advice.

Important notice: this document has been prepared for professional investors and has been approved as a financial promotion by Downing LLP (“Downing”). Capital is at risk and investors should note that their investments and the income derived from them can fall as well as rise and investors may not get back the full amount invested. Downing does not offer investment or tax advice or make recommendations regarding investments. Downing is a trading name of Downing LLP. Downing LLP is authorised and regulated by the Financial Conduct Authority (Firm Reference No. 545025). Registered in England and Wales (No. OC341575). Registered Office: 10 Lower Thames Street London EC3R 6AF.

.jpeg)