None of the information provided is investment or tax advice. You should always read the associated risks before deciding whether to invest. These can be found on the product pages as well as in our risks overview. Please confirm you have read the information above.

The defensive parts of a multi‑asset portfolio are essential for protecting investors during market stress, even though we believe equities remain the strongest long‑term guardian of purchasing power.

Cash is now an effective, low‑cost defensive tool across both inflationary and deflationary shocks, while gilts now offer recession‑protection potential. Corporate and high‑yield bonds look unattractive.

Gold is a great long-term defender but can be capricious over shorter periods (which still matter). The risk of over-crowding has also grown after recent price spikes.

Downing launches new actively managed liquid alternatives fund aiming to deliver 7% to 10%+ per annum and positive returns in most markets. The new MGTS Downing Active Defined Return Assets Fund (‘Active Defined Returns’, the ‘Fund’), is the first fund from its new Liquid Alternatives team.

The Fund is aimed at institutional investors, Discretionary Fund Managers, IFAs and advised sophisticated individual investors, and will primarily consist of UK Government bonds and large-cap equity index options, which provide significant scalability and strong liquidity. It aims to deliver 7% to 10%+ per annum and positive returns in all markets except for a sustained equity market fall (generally more than 35%), over a period of at least six years.

The Fund is the first to be launched by the new Liquid Alternatives Team established by Downing. Collectively, the team has over 125 years of experience and sector knowledge, and includes Tony Stenning, who held senior roles at BlackRock and most recently was CEO of Atlantic House Group; Russell Catley, founder and also a former CEO of Atlantic House Group; Huw Price, a former Executive Director at Santander Asset Management, and Paul Adams, former Head of Cash Equities and Derivatives Sales, Royal Bank of Canada.

The Fund offers investors a compelling building block for multi-asset portfolios, aiming to add consistent and predictable returns, typically secured with a portfolio of UK Government bonds. The unique proposition includes a hybrid approach of using systematic derivative strategies and active management, combining liquid investments with predictable returns, and an equity like risk profile.

Investment strategy: Maximising the probability of delivering predictable defined returns across the economic cycle.

Systematic Liquid Derivatives: Systematic, derivative strategies optimise the equity risk-return profile. The Fund uses rules-based derivative strategies linked to the most liquid, large-cap global equity indices (i.e. FTSE100, S&P500) with the aim of harvesting well-proven consistent returns across a wide corridor of market conditions.

Strong security: The Fund will hold a high-quality portfolio of assets as secure collateral – typically UK Government bonds.

Active benefits: At times, rules-based, passive derivative strategies can underperform when markets move strongly – this is when specialist active management can add incremental gains by monitoring and monetising positions and applying active risk management.

Key benefits

Increased consistency and predictability of returns: Positive returns in all markets except for a sustained equity market fall of more than 35% over at least six years.

Diversification of risk: The Fund’s risk components are diversified across large, liquid equity indices, observation levels and counterparties. Secured with high-quality assets – typically UK Government bonds.

Active management: Our experienced team will actively manage the Fund and its investments to optimise risk and reward for investors.

Russell Catley, Head of Retail, Liquid Alternatives at Downing, said: “Put simply, we focus your investment risk on the probability of receiving the returns you need, not those you don’t. We target the highest probability of delivering 7% to 10%+ per annum with active management adding material incremental gains. We believe that we are building the next evolution of the proven success of Defined Returns funds

The Downing team isseeing strong demand from clients looking for alternatives to large-cap equity funds which are becoming concentrated in technology stocks, or alternatives to UK equity income funds and illiquid alternatives.”

Tony Stenning, Head of Liquid Alternatives at Downing, said: “The launch of our Active Defined Return Assets Fund is a significant milestone in the ambitious build-out of our new Liquid Alternatives strategies. It is a solution-focused fund that should deliver stable high single or low double-digit returns across a wide spectrum of equity market conditions, except for a persistent multi-year bear market. The Fund is designed to enhance balanced portfolios by providing consistent, predictable returns and is suitable for accumulation or drawdown.

“We aim to deliver a unique combination of proven systematic derivative strategies and specialist active management, and we are doing so at a very compelling fee level, below our closest competitors and in line with active ETFs.”

How the Fund is expected to perform in different markets

In bullish markets: UK Government bonds secure the capital, and the equity index options deliver a predictable 7-10%+ return per annum – giving up some less likely upside.

In neutral markets and normal market corrections: UK Government bonds secure the capital, and the index options deliver a predictable 7-10%+ return per annum.

In a sustained sell-off: if markets fall more than the cover to capital loss and do not recover for six years. Then capital is eroded 1:1 in line with the worst performing index.

The average Cover to Capital Loss is targeted at 35%: the average cover to capital loss represents the average level the Global indices within the Fund could fall before capital is at risk.

Fund key risks

Performance: Capital is at risk. Investors may not get back the full amount invested.

Liquidity: Access to capital is always subject to liquidity.

Counterparty risk: Other parties could default on the contractual obligations.

Fund Structure

UK regulated OEIC fund structure, fully UCITS compliant

Daily dealing, at published NAV

Minimum investment: £100,000

SRRI: 6 out of 7

Depositary: Bank of New York

Authorised corporate Director (‘ACD’): Margetts Fund Management Ltd.

I share-class: SEDOL: BM8J604 / ISIN: GB00BM8J6044

F share-class: SEDOL: BM8J615 / ISIN: GB00BM8J6150

Risk warning: Opinions expressed represent the views of the fund manager at the time of publication, are subject to change, and should not be interpreted as investment advice. Please refer to the latest full Prospectus and KIID before investing; your attention is drawn to the risk, fees and taxation factors contained therein. Please note that past performance is not a reliable indicator of future results. Capital is at risk. Investments and the income derived from them can fall as well as rise and investors may not get back the full amount invested. Investments in this fund should be held for the long term.

Important notice: This document is intended for professional investors and has been approved as a financial promotion in line with Section 21 of the FSMA by Downing LLP (“Downing”). This document is for information only and does not form part of a direct offer or invitation to purchase, subscribe for or dispose of securities and no reliance should be placed on it. Downing does not offer investment or tax advice or make recommendations regarding investments. Downing is a trading name of Downing LLP. Downing LLP is authorised and regulated by the Financial Conduct Authority (Firm Reference No. 545025). Registered in England and Wales (No. OC341575). Registered Office: 10 Lower Thames Street, London EC3R 6AF.

The Art of Defence

It’s hard to look away from stock markets, but the non-equity parts of a multi-asset portfolio are just as important. Within the Fox Funds, we call these the ‘Defence’ component, because we see that function – defending in the bad times – as the main reason for holding this stuff. And with one protective option – gold – on an absolute tear this year, this is a good time to run through the runners and riders when it comes to investment defence.

What’s the point?!

It’s easy to lose sight of this amid the blood and thunder of markets, but the point of investing is to ‘store’ wealth we don’t need today in something that - when we do need it in five/ten/whenever years’ time - will buy us at least the same amount of goods or services as when we started (and ideally more). Clearly this is easier said than done: Largely because the best investments for doing that over the long-term are often painfully volatile in the short-term, which means that some investors can’t hold them (they don’t have the stomach for it or their timeframe is too short).

This leads to what I’d call a Double-DIYD problem (damned if you do, damned if you don’t): If you try to defend against short-term threats, you’ll lose out in the long-term, but if you try to protect against long-term damage, you’ll lose out in the short-term.

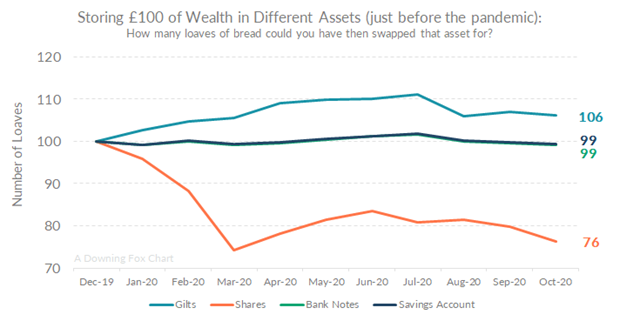

I’ll show you what I mean. The following charts measure investment performance not in money terms, as that can play tricks, but in bread terms. Because if you invest in an asset for ten years and it rises in money terms - but now buys you less bread than when you started - it’s probably been a bad investment, no matter what the pound signs tell you. We’ll start with an example of the short-term, using the pandemic experience of 2020:

Source: ONS, CPI Index Bread & Morningstar, 31.12.2019 to 31.10.2020. Past Performance is not a reliable indicator of future returns.

Assuming a loaf of bread cost about £1 at the end of 20191, you can see the outcome of taking £100 of your wealth and storing it four different ways: In a UK equity tracker; a UK gilt tracker; a high-street savings account; or stuffing the bank notes under your mattress.

As the period began, your £100 of wealth could buy you 100 loaves. Looking at the bank notes first, you can see the point of using bread to measure investment performance: Those five £20 notes still add up to 100, but because the price of bread rose slightly over this period they ended being swappable for 99 loaves, not 100. In essence, you’ve become just a little bit poorer. It’s then a similar story for the savings account, as they paid little more interest than a bank note did back then.

Gilts, meanwhile, showed their defensive mettle: As panic set in, more investors bought them, pushing their prices up. So they didn’t just protect your bread-buying ability, they actually boosted it (by six loaves). Equities, in contrast, were a disaster. This was because the stock market crashed in the pandemic, and in just ten months your purchasing power dropped from 100 loaves to 76. If it carries on like that for much longer, many reasoned, I’ll be out of the bread-buying market for good. So, on the basis that 76 loaves of bread are better than none, they sold their shares, locking in their new level of poverty.

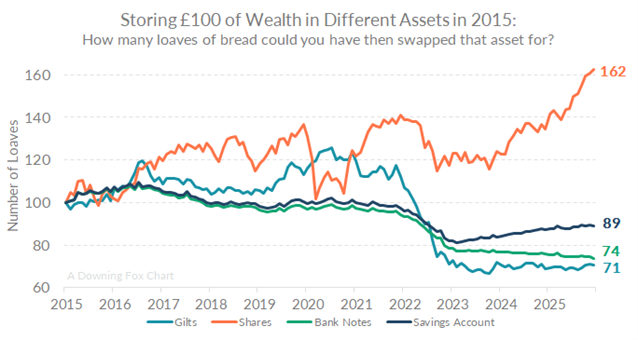

It's episodes like this that puts many risk-averse investors off holding equities. And this is the problem: Over longer periods, including the last ten years (which contained not just the pandemic, but also Brexit, Ukraine and both Trump presidencies), they have been - by a very wide margin – the most defensive of these four choices:

Source: ONS, CPI Index Bread & Morningstar, 31.01.2015 to 31.12.2025. Past Performance is not a reliable indicator of future returns.

This chart, remember, is now showing two things: What happened to the prices of those assets and to the price of bread. So the green line – bank notes – is falling, but that’s only because the price of bread is rising. If the chart was measuring progress in money terms rather than baked goods, that line would be dead flat. That it falls steeply in 2022 illustrates the return of inflation, which came roaring back from the dead as the prices of real things – like bread – rose sharply.

It is this factor; inflation, that’s the silent, long-term killer. It’s usually eating away at the buying power of your bank notes in a small way, which means it doesn’t show up in short-term data, and then – every now and then – it shows up in a large way too. You’ll note that savings accounts followed roughly the same path until interest rates were hiked upwards in 2023, since when they’ve clawed back some of your Hovis-buying capacity.

Gilts, however, have had a shocker. Ten years after making your investment, you can now only buy 71 loaves of bread. This is down to a double whammy: The price of bread has inflated by 35%, while the price of your gilts has shrunk by 5% (not a coincidence: bonds hate inflation like cats hate water).

Now look at your equities: they’re now worth 162 loaves! The cost of bread may have risen sharply, but the value of your shares has risen further, so you’re rolling in the stuff! You could eat as much bread as you wanted and still have enough to bathe in a tub of leftover crumbs2.

The best form of defence?

This is why I personally like equities as long-term protectors3; because sometimes attack is the best form of defence. The reason why this works is – broadly - that companies are always trying to grow their profits. They might get caught out in the short-term by a burst of inflation, but the management teams of those companies will then do everything they can to restore lost profits. And while not every company will succeed, collectively they probably will, and when they do it’s likely the price of those shares will rise back to reflect that.

In other words, unlike a bond, the dividends a company pays you (or the price you can sell its shares for) are not fixed but are instead linked to its profits (by an admittedly long and stretchy piece of elastic). And for an optimist like me, that’s actually a good thing and not a reason to run for the hills.

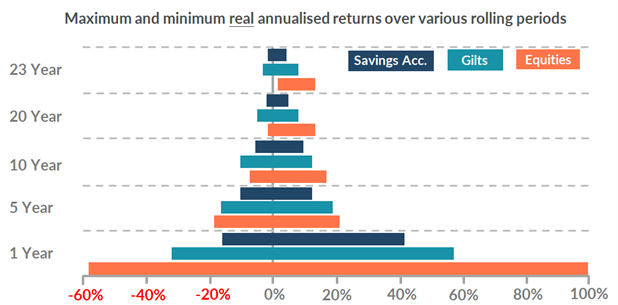

The following chart, which is one of my all-time favourites (props to the good folk of Barclays), shows this short-term vs long-term trade-off. Using historical UK data, it sets out the range of outcomes in annualised real terms (i.e. per year, after inflation) for three different asset classes: a savings account; gilts; and shares.

Source: Barclays 2018 Equity Gilt Study and Downing Fox. Past Performance is not a reliable indicator of future returns.

You can see that, if you’re investing for just a year, the historical range of outcomes for all three asset classes is wide, but for equities it’s extreme: Sure, in the best year you made 100%, but in the worst you lost over half your money. And if you’ll need your money back in a year, investing in an asset class that could make you a big loss is a bad idea. This is what scares off the risk-averse investor, even if they have a ten-year horizon.

But as your investment horizon grows, that range of outcomes narrows dramatically. By extending to five years, there’s not much difference between equities and gilts, and by the time you’ve stretched to a ten-year holding period, equities – on a historical basis – have actually been the lower risk option compared to gilts (as well as the one that produced the highest returns in the good times).

This is why I’m personally happy to rely on equities. But obviously not everyone can do the same. My own time horizon is at least 15 years, but some can’t stretch that long. And no matter how well you explain the logic, the reliable long-term is still made up by a series of unreliable short-terms, and the risk-averse simply can’t handle those short-term swings of the market.

Surviving short-term storms

For these folk, then, we need to find some way of making the short term more bearable. This means using non-equity assets to reduce the short-term volatility of their portfolio. Clearly the best asset to hold when equities are falling would be one that goes up, followed by one that stands still, then – at the very least – one that falls by less than equities. If your multi-asset manager’s defensive exposure falls by more than equities in a crash (see 2022), then they’ve failed: Send them to jail without passing Go.

Now, wouldn’t it be lovely if we could just pick an asset off a shelf that reliably rose in each and every equity sell-off?

The closest we can get to this is cash which should always stand still in nominal terms4. But this will look a weak defence if everyone else is holding defensive assets that rise during that crisis. Under these circumstances, it will look like you were taking more risk by holding cash, not less. And no matter how much we deny it, appearances matter. To give you an idea of how that looks, I’ve included a few charts of how different defensive assets performed in two very different sell-offs: the 2008 financial crisis (a deflationary sell-off) and then 2022 (an inflationary sell-off).

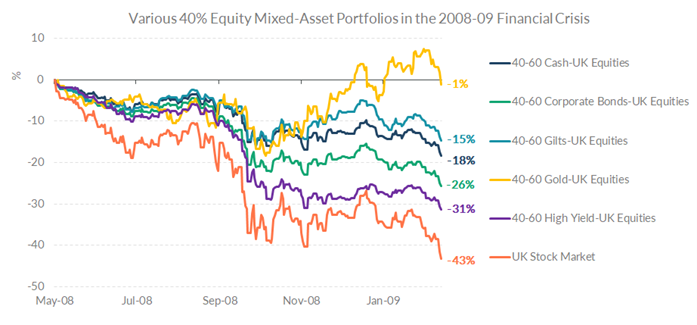

Each chart shows how five portfolios, each consisting of 40% UK Equities mixed with 60% of a different defensive asset would have fared in each crisis.

The Global Financial Crisis

We’ll start with the peak-to-trough experience for 2008’s financial crisis. This was a brutal time for equities. At their worst, UK equities fell by 43%. Any of the popular diversifiers we’ve included here would have helped cushion the blow, but clearly some did better than others.

Cash helped, but using assets that sharply rose in price, like gilts or gold, would have produced an even more defensive result for your nervy investors. Meanwhile corporate bonds (higher-quality bonds issued by companies) and high-yield bonds (lower quality corporate bonds) diluted, but because they fell in price, they proved far weaker defensive counterbalances than the first three.

Source: Morningstar, 19.05.2008 to 03.03.2009. Past Performance is not a reliable indicator of future returns.

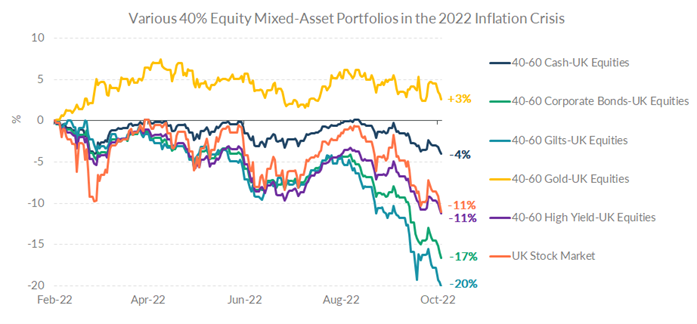

The Inflationary Crisis of 2022

The most obvious difference with the 2022 market panic was that some defensive choices actually made the problem worse. Both gilts and corporate bonds fell by more than equities, which meant some multi-asset fund ranges produced the steepest falls for their supposedly lower-risk options: A huge no-no in the financial planning world.

Cash fared OK by standing still, while equities went backwards. Gold proved the standout defender again, rising by enough to give that particular 40-60 portfolio a positive outcome despite negative conditions.

Source: Morningstar, 10.02.2022 to 12.10.2022. Past Performance is not a reliable indicator of future returns.

With that history set out, I thought I’d run through these options as short-term defenders (as separate from being a long-term defensive options - see the opening paragraphs on equities). I’ll do this both in general terms and specifically with reference to how they’re set up as defenders today.

Cash

In terms of reliability, cash is hard to beat as a defender against a short-term shock. It’s particularly useful as nobody knows if the next crisis will be inflationary like 2022, or deflationary like 2000 or 2008. It doesn’t much matter to cash though, as it’ll do roughly the same thing in either scenario.

Given this, and the fact that it’s low cost, it’s suspiciously under-used by multi-asset portfolio managers. I imagine this is because it’s harder to justify charging a management fee for something many retail investors feel they could do themselves. We like it though, especially as we’re being paid reasonable interest to hold it in a way we weren’t back in 2022. Today we hold more than two-thirds of our Defence Component in cash or cash-like assets (we avoid the awkward “why are you charging us for holding cash?!” questions by not charging you for holding cash5).

It's worth nothing that a reasonable minority of our exposure is held in overseas currencies (yen, euros and dollars), as we think these can also serve as useful defenders for British investors in times of stress (holding a fistful of dollars was part of the reason we defended so well in 2022). But in the interests of wordcount, I won’t get into that here.

Longer-duration gilts/government bonds

These are tricker ponies than cash. If it’s deflation that’s bugging the equity market (i.e. a recession), they have a good chance of going up in price, thereby acting as better defenders. But if it’s inflationary, which means the prices of ‘stuff’ is rising more quickly than the fixed principal and coupons of gilts, they can head south at precisely the time you don’t want them too.

Like most assets, their starting level matters too. Generally, the lower their yield when the recession hits, the weaker their defensive bounce is likely to be. This made them an easy ‘avoid’ in 2022, as their yields were close to zero, meaning they had little defensive power in a recession, and massive potential downside in inflationary spike. In other words, there was no good reason for holding them, which is why we didn’t. But today, with yields in the neighbourhood of 4.5%, they’re more finely balanced, and we have about a third of our defensive exposure held in them.

Corporate bonds

This is one of the biggest differences between us and our peers. We never hold these assets, as they don’t suit our polarised investment model. By that I mean they’re not growthy enough for our Growth Component, as they don’t go up as much as equities in the good times. And they’re not defensive enough for our Defence Component in the bad times: Yes; they generally hold up better than equities (although not in 2022), but they’re still likely to fall in a crisis and are therefore less useful than cash.

Where they are useful is in those mild sell-offs that you might see two or three times a year – where the stock market drops by, say, 5% and then recovers. This is because corporate bonds tend not to join the retreat until things get really bad. But we believe these short-lived non-events matter less to you than the really bad events, as most retail investors won’t know about a stock market sell-off until it hits the ten o’clock news. And by that stage corporate bonds are probably falling too.

There are also better and worse times to hold them. It’s generally a better idea to hold them when they’re yielding a lot more than government bonds (“wide spreads”), as this suggests they’ll have less far to fall in a reversal. Today, however, yields are about as close to the government bond equivalents as they’ve been in a lifetime, suggesting a high risk of “spreads blowing out” if the economy starts to creak. So even if we could hold these bonds, we certainly wouldn’t be holding any today.

High-yield bonds

Everything I’ve said about corporate bonds above applies to high-yield bonds, but more so. These are bonds issued by wobblier companies, so are naturally riskier than their ‘investment-grade’ peers. The one quirk is that they tend to fare less badly if inflation is the problem (see 2022), as these are often highly indebted companies and – ironically – the right type of inflation might actually improve their chances of survival by inflating some of that debt away.

Many of our peers use these as defenders, but I really don’t think they qualify for that label: If we were ever to hold them, it would be more appropriate to include them next to equities on account of their potential to fall steeply in a crisis.

Gold

As you can see from the previous charts, gold has been the outstanding defensive asset of the last few sell-offs. If I have one regret about how I set up the Downing Fox portfolios, it’s that I didn’t include gold6 in the range of assets they’re permitted to hold. This has meant we don’t have this defender as an option, and we’ve also missed out on its meteoric rise of the last few years.

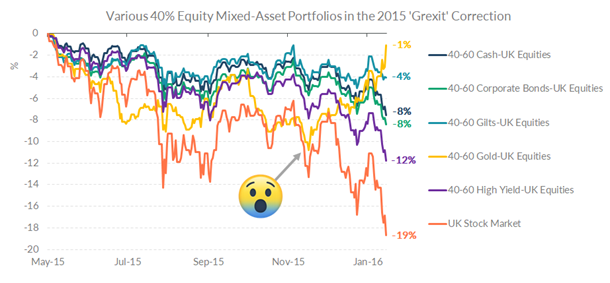

This was based on my view that, a bit like equities, I like gold as a fantastic long-term defender of your buying power, but as a protector against short-term problems, it can be a little more capricious. To illustrate, it’s useful to have a look at the stock market retreat of 2015, which was caused by rising concerns over the risk of Greece leaving the EU (dubbed ‘Grexit’ - little did we know…).

Source: Morningstar, 28.05.2015 to 11.02.2016. Past Performance is not a reliable indicator of future returns.

As you can see, the eventual outcome for the gold-bolstered portfolio was good – even compared to cash or gilts. But if you’re trying to keep twitchy retail investors on their financial path, the journey matters too. And there was a point (marked on the chart) when you were seven months into a bleak, falling market and nursing a double-digit loss on your equities. This is a long time when you’re living it, and holding gold as your only defender wouldn’t have helped (even high-yield bonds were holding up better), raising the chances that a cautious investor would abandon ship at a financially damaging moment.

Gold is also even harder to predict than gilts, as it doesn’t produce a stream of income by which you can judge if it’s become dangerously expensive or not. This raises the risk of falling foul of what financial folk call a ‘Minsky Moment’ (and everyone else calls Sod’s Law). Where an asset does so well as a defender over repeated episodes that everyone buys it, it leaves no one to buy it in the event of an emergency, which means its price will no longer rise when panic sets in, and may even drop. Put another way, the more popular an asset gets for doing well as a low-risk option, the riskier it becomes (see gilts in 2022).

Are we at such a point today?

I don’t know. That lack of an income stream to judge makes it impossible to be certain. I still like it as a long-term store of wealth, particularly as inflation seems like the most likely answer to the world’s growing debt problem (which wouldn’t bode well for fiat currencies). But after such a quick, steep rise, I’d be concerned that it might actually join in with a risk-off move, thereby failing as a short-term defender within a portfolio.7

The round-up

To summarise: For long-term investments, I still like equities, although I’d want to make sure they’re not overvalued (and large parts of an equity index appear that today, but thankfully we can be selective). Gold looks good too, although we don’t own it for the technical reasons mentioned above.

But if you need to guard against short-term bouts of volatility in either of those assets, cash looks like a decent option – especially as you’re still being paid an inflation-like amount for holding it (just about, for now). Gilts seem OK and should do you proud in a recession-driven market, although they’ll still struggle if inflation wins out (which over the long term it may well do). Some overseas currencies may also provide insurance-like performance in a panic, and we like the Japanese yen for that.

But I can’t see much point in holding corporate bonds as defenders today, so I’m entirely comfortable with our complete avoidance of them (this position is not common to most of our peers).

As always, there’s so much more I could say on this subject, but I’ve taken enough of your time already. If you’d like to know more, you know where we are.

1 Which it did, unless you were buying posh artisanal loaves (which - full confession - I was. I still am too: Life’s too short for crappy bread). 2 Not recommended. 3 Almost all of my own investable wealth is held in The MGTS Downing Fox 100% Equity Fund. 4 As opposed to after inflation – “real terms” - which can occasionally see a sharp drop in the real value of cash – like 2022. 5 The MGTS Downing Fox fund charges effectively only reflect the amount held in equities, with the rest – the mix of cash and bonds held in the Defence Component – managed by us for free. 6 Or at least technically a gold-linked ETF. 7That said, I’m exploring the possibility of adding gold to our roster of potential defensive holdings. I’ll let you know if we do.

Opinions expressed represent the views of the fund manager at the time of publication, are subject to change, and should not be interpreted as investment advice.

Important notice: this document has been prepared for professional investors and has been approved as a financial promotion by Downing LLP (“Downing”). Capital is at risk and investors should note that their investments and the income derived from them can fall as well as rise and investors may not get back the full amount invested. Downing does not offer investment or tax advice or make recommendations regarding investments. Downing is a trading name of Downing LLP. Downing LLP is authorised and regulated by the Financial Conduct Authority (Firm Reference No. 545025). Registered in England and Wales (No. OC341575). Registered Office: 10 Lower Thames Street London EC3R 6AF.

.jpeg)

.png)