None of the information provided is investment or tax advice. You should always read the associated risks before deciding whether to invest. These can be found on the product pages as well as in our risks overview. Please confirm you have read the information above.

Market context & paradigm shift: Global markets may have transitioned from a phase resembling the pre-tech bubble era to one akin to the post-bubble crash of the early 2000s.

The life cycle of a megatrend: Investment megatrends go through a ten-stage cycle from “Unthinkable”, through “Popular”, to “Forgotten.” The Commodity Super cycle of the 00s provides a clear example of this.

Current megatrend: American exceptionalism: We believe this may have moved from Stage 7 (Questionable) to Stage 8 (Worrisome) – this could have serious implications for many commonly-held investments.

Downing launches new actively managed liquid alternatives fund aiming to deliver 7% to 10%+ per annum and positive returns in most markets. The new MGTS Downing Active Defined Return Assets Fund (‘Active Defined Returns’, the ‘Fund’), is the first fund from its new Liquid Alternatives team.

The Fund is aimed at institutional investors, Discretionary Fund Managers, IFAs and advised sophisticated individual investors, and will primarily consist of UK Government bonds and large-cap equity index options, which provide significant scalability and strong liquidity. It aims to deliver 7% to 10%+ per annum and positive returns in all markets except for a sustained equity market fall (generally more than 35%), over a period of at least six years.

The Fund is the first to be launched by the new Liquid Alternatives Team established by Downing. Collectively, the team has over 125 years of experience and sector knowledge, and includes Tony Stenning, who held senior roles at BlackRock and most recently was CEO of Atlantic House Group; Russell Catley, founder and also a former CEO of Atlantic House Group; Huw Price, a former Executive Director at Santander Asset Management, and Paul Adams, former Head of Cash Equities and Derivatives Sales, Royal Bank of Canada.

The Fund offers investors a compelling building block for multi-asset portfolios, aiming to add consistent and predictable returns, typically secured with a portfolio of UK Government bonds. The unique proposition includes a hybrid approach of using systematic derivative strategies and active management, combining liquid investments with predictable returns, and an equity like risk profile.

Investment strategy: Maximising the probability of delivering predictable defined returns across the economic cycle.

Systematic Liquid Derivatives: Systematic, derivative strategies optimise the equity risk-return profile. The Fund uses rules-based derivative strategies linked to the most liquid, large-cap global equity indices (i.e. FTSE100, S&P500) with the aim of harvesting well-proven consistent returns across a wide corridor of market conditions.

Strong security: The Fund will hold a high-quality portfolio of assets as secure collateral – typically UK Government bonds.

Active benefits: At times, rules-based, passive derivative strategies can underperform when markets move strongly – this is when specialist active management can add incremental gains by monitoring and monetising positions and applying active risk management.

Key benefits

Increased consistency and predictability of returns: Positive returns in all markets except for a sustained equity market fall of more than 35% over at least six years.

Diversification of risk: The Fund’s risk components are diversified across large, liquid equity indices, observation levels and counterparties. Secured with high-quality assets – typically UK Government bonds.

Active management: Our experienced team will actively manage the Fund and its investments to optimise risk and reward for investors.

Russell Catley, Head of Retail, Liquid Alternatives at Downing, said: “Put simply, we focus your investment risk on the probability of receiving the returns you need, not those you don’t. We target the highest probability of delivering 7% to 10%+ per annum with active management adding material incremental gains. We believe that we are building the next evolution of the proven success of Defined Returns funds

The Downing team isseeing strong demand from clients looking for alternatives to large-cap equity funds which are becoming concentrated in technology stocks, or alternatives to UK equity income funds and illiquid alternatives.”

Tony Stenning, Head of Liquid Alternatives at Downing, said: “The launch of our Active Defined Return Assets Fund is a significant milestone in the ambitious build-out of our new Liquid Alternatives strategies. It is a solution-focused fund that should deliver stable high single or low double-digit returns across a wide spectrum of equity market conditions, except for a persistent multi-year bear market. The Fund is designed to enhance balanced portfolios by providing consistent, predictable returns and is suitable for accumulation or drawdown.

“We aim to deliver a unique combination of proven systematic derivative strategies and specialist active management, and we are doing so at a very compelling fee level, below our closest competitors and in line with active ETFs.”

How the Fund is expected to perform in different markets

In bullish markets: UK Government bonds secure the capital, and the equity index options deliver a predictable 7-10%+ return per annum – giving up some less likely upside.

In neutral markets and normal market corrections: UK Government bonds secure the capital, and the index options deliver a predictable 7-10%+ return per annum.

In a sustained sell-off: if markets fall more than the cover to capital loss and do not recover for six years. Then capital is eroded 1:1 in line with the worst performing index.

The average Cover to Capital Loss is targeted at 35%: the average cover to capital loss represents the average level the Global indices within the Fund could fall before capital is at risk.

Fund key risks

Performance: Capital is at risk. Investors may not get back the full amount invested.

Liquidity: Access to capital is always subject to liquidity.

Counterparty risk: Other parties could default on the contractual obligations.

Fund Structure

UK regulated OEIC fund structure, fully UCITS compliant

Daily dealing, at published NAV

Minimum investment: £100,000

SRRI: 6 out of 7

Depositary: Bank of New York

Authorised corporate Director (‘ACD’): Margetts Fund Management Ltd.

I share-class: SEDOL: BM8J604 / ISIN: GB00BM8J6044

F share-class: SEDOL: BM8J615 / ISIN: GB00BM8J6150

Risk warning: Opinions expressed represent the views of the fund manager at the time of publication, are subject to change, and should not be interpreted as investment advice. Please refer to the latest full Prospectus and KIID before investing; your attention is drawn to the risk, fees and taxation factors contained therein. Please note that past performance is not a reliable indicator of future results. Capital is at risk. Investments and the income derived from them can fall as well as rise and investors may not get back the full amount invested. Investments in this fund should be held for the long term.

Important notice: This document is intended for professional investors and has been approved as a financial promotion in line with Section 21 of the FSMA by Downing LLP (“Downing”). This document is for information only and does not form part of a direct offer or invitation to purchase, subscribe for or dispose of securities and no reliance should be placed on it. Downing does not offer investment or tax advice or make recommendations regarding investments. Downing is a trading name of Downing LLP. Downing LLP is authorised and regulated by the Financial Conduct Authority (Firm Reference No. 545025). Registered in England and Wales (No. OC341575). Registered Office: 10 Lower Thames Street, London EC3R 6AF.

Did we just enter a new investment paradigm?

I’ve been banging on for ages about how markets are acting like they did before the tech bubble burst in 2000. The good news is that I might be able to stop doing that now. The bad news? It’s because markets are suddenly acting like they did after it burst. And that wasn’t pretty.

Question number one, then, is why do I feel like we’ve moved from ‘before’ to ‘after’?

To borrow from The Castle - one of the 20th Century’s greatest works of art – I’d say “it’s the vibe”1. I’ll concede that this alone may not be enough to warrant ripping up your high-flying portfolio, so I’ll expand.

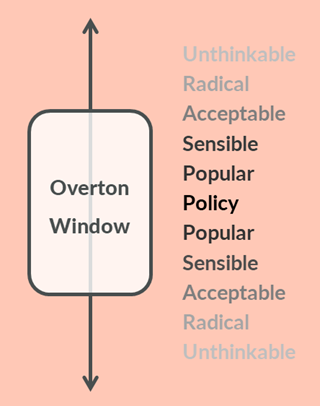

At any given moment, ‘the vibe’ is contained by something called the Overton Window. In politics, this describes the collection of political views that range from acceptable to popular, with everything else – the unpopular and the unacceptable - sat outside the window. This window moves over time, usually slowly, but sometimes suddenly, such that a view can transition from being unthinkable in one year to being popular in another. Take the topic of immigration control in the UK: For a centrist politician like Keir Starmer, being ‘for’ this was unthinkable ten years’ ago, yet today he’s (politely) proposing anti-immigration policies.

It's a useful concept for investing too. We call it ‘The Consensus’ and, like the Overton Window, it moves around – sometimes gradually, sometimes dramatically. When I think back to 2010, I recall the Window then containing beliefs such as ‘emerging markets always outperform’; ‘commodities are great diversifiers’; and ‘oil’s going to $200’.

At the same time, investing in tech companies was basically unthinkable. It was only superfans like Baillie Gifford’s James Anderson, along with a few contrarian value managers (Microsoft was an unloved value stock in 2010) who were making the case for it. Such investors were breezily dismissed as cranks or relics from a lost era.

Clearly the consensus changed. But how did that happen?

From birth to death, there are ten stages a megatrend passes through. Here, through the lens of the huge ‘Commodity Supercycle’ consensus of the noughties, are those ten stages:

1. Unthinkable: Commodities, and associated assets like emerging market equities, are available, but nobody’s interested. Largely because they’re obscured by the prevailing tech megatrend, but also because of earlier poor performance.

2. Radical: One or two investors see the potential of holding commodities and begin to make their case. They are widely ignored, with all eyes remaining on the high-flying tech megatrend.

3. Acceptable: As we move from 1999 into 2000, the old consensus on tech is beginning to wobble, as volatility has risen and valuations look high. Adding some commodities as diversifiers doesn’t sound quite so leftfield, although few investors are willing to act.

4. Sensible: The tech consensus has collapsed, causing steep losses. In contrast, investing in almost anything else, including commodities and emerging markets, looks like a sensible thing to have done. We are now in a period of benign chaos (the early noughties) where there is no single winning consensus trade (other than ‘avoid tech’) while the world works out what comes next.

Past performance is not an indication of future performance. Source: FE Analytics, Total Return 29.12.1989 (start of data) to 31.12.2019 (Numbers are: 29.12.89 to 31.08.98; 31.08.98 to 11.04.11; and 11.04.11 to 31.12.19)

5. Popular: From the chaos emerges a new consensus on commodities. This is because they’ve performed well and they have a compelling narrative (this was when the world noticed how big China was, how fast it was growing, and the volume of commodities it would require). Nicknames and acronyms (‘Commodity Supercycle’ and ‘BRICs’) emerge and catch on, driving more interest, which further drives performance, creating a positive feedback loop.

6. Consensus: The story becomes so well known, and the performance so compelling, that commodities are now taken as a core asset to which you should always have high exposure. Their winning streak also makes them large weightings within index-tracking products (in 2010, Exxon was the world’s biggest company, and therefore the largest position in a global tracker).

7. Questionable: Into the new decade (the 2010s), and commodities still dominate the headlines, but volatility has risen, valuations look high, and there have been a couple of short-but-heart-stopping falls. They remain popular, particularly among retail investors, but the dissenting voices are growing, and doubts are creeping in.

8. Worrisome: There has been a more serious fall accompanied by signs of deterioration in the fundamentals. This has caused many previously enthusiastic holders to start seeing the glass as half empty, not half full. But prices are rebounding, so while institutional investors might edge back from the trade, they’re not fully abandoning it yet.

9. Abandoned: The earlier rebound proved temporary, and prices have plunged to new lows. It’s clear the game is up, so now professional investors don’t want you seeing it in their portfolio and raise their pace of selling. This is when previously willing proponents explain how they saw this coming all along.

10. Forgotten: The circus has moved on (back to tech in this case, and the emerging consensus around American exceptionalism and the FAANGs / Magnificent Seven). The remnants of the Commodity Supercycle megatrend are deleted from portfolios, while many of the natural resources funds launched during the consensus are quietly shuttered (or converted into ESG funds).

Where are we now?

The reason I’m saying this now is that, thanks to President Trump and Liberation Day, it feels like the prevailing consensus has suddenly shifted. Specifically, it’s moved from Stage 7 (Questionable) – to Stage 8 (Worrisome). This is not a fun stage, particularly if you’re heavily exposed to it.

We’ll call this consensus ‘American exceptionalism’ (which was in Stage 1 – unthinkable - back in 2010), but it incorporates other factors such as tech, mega-caps, and AI. Here are some reasons why I think it’s shifted to Stage 8:

• I wrote my last quarterly letter early in February about how ‘home bias’ might not be such a crazy idea for us Brits, and how exposing two thirds of your portfolio to American equities was the bigger risk. It seemed radical when I wrote it, but just three months later it’s become acceptable.

• As 2025 began, a risk analyst at a large Swiss pension scheme would have tapped a portfolio manager on the shoulder for ‘only’ holding 65% US equities when the benchmark suggested 70%. Today, the same risk analyst will be roasting the manager for holding a ridiculously high 65% of their clients’ wealth in a volatile foreign country whose markets are underperforming.

• Because yes; the macro view has changed. The US now seems hostile, unpredictable, and much less of an ally. They’ve also stated that they want to meaningfully weaken the dollar. At the same time, withdrawal of US support has caused Germany, which is about to turn on its fiscal spigots (finally!), to go from being Europe’s handbrake to its accelerator pedal.

• The big beneficiaries of globalisation have been US companies and the US dollar. It’s not a stretch, therefore, to imagine that the big losers from the de-globalisation trend might be US companies and the US dollar.

• The new macro narrative is backed by some compelling performance numbers, driven by the impact of US equities and the US dollar falling simultaneously (until this year, the dollar had generally risen when US equities fell). Since the market peaked in January2, British holders of an S&P500 tracker have lost around 9%, whereas a UK equity tracker has risen by about 3%. Most countries around the world have experienced something similar. This is likely to encourage non-US capital to be pulled back home from the States.

• An American investor, meanwhile, is looking at a 2% loss from the S&P500. This doesn’t seem that bad, but because sterling has risen against the dollar and the UK index has outperformed, the 11% they could have made in British equities looks much better (as, again, does the return made by many other non-US markets). So, for the first time in years, American investors will be questioning the decision to invest all their money at home when they could be diversifying into rallying foreign markets.

• If I’m right about this (and I may well not be), then such shifts out of the US are only going to exacerbate these performance trends, which will encourage further moves away. This is how feedback loops begin. It was a feedback loop that drove the US exceptionalism megatrend over the last decade, and it may well be an equal and opposite feedback loop that deflates it over the next decade too.

What to do?

This begs the following question: If I am right about this, why not just sell all your equities and run for the hills?

The obvious response is that I might not be right: The world could well go back to the way it was, American mega-caps will keep winning, and you will curse the day you ever read this letter.

My second response is because inflation is still a big threat, and equities are – in my opinion – the best long-term bet for protecting your wealth against it. Unless, that is, they’ve become dangerously expensive. In which case, a de-rating of a company’s share price might cancel its inflation-beating profit growth.

However, there are large swathes of the global equity market that, having been on the wrong side of the American exceptionalism megatrend for a decade, are far from dangerously expensive. But you will need to be active to find these, because classic passive funds, having played their part in exacerbating the American exceptionalism trend, look likely to suffer when it unwinds (in my opinion, naturally. Other opinions are available).

For the record, almost all my investable wealth is aligned with my second response, by which I mean it’s invested in our Fox 100% Equity Fund (which is 100% actively managed).

What could this market phase look like?

Assuming I’m right on this (to reiterate, this is a significant assumption), it might be useful to know how Stage 8 of a megatrend looks close up. So, to provide a useful historical example (while wilfully misquoting Jarvis Cocker); let’s all go back to the year 2000.

2000 was the year the tech bubble peaked and it was also the start of a nasty three-year bear market for global equities. It’s useful to see how that year unfolded, because if this is a re-run you need to know two things: Firstly, it was the start of a truly painful period for some (but not all) investors - 25 years later, many still haven’t forgiven their advisers for mistakes made. And secondly, much as it seems clear that - in hindsight - we’d entered a bear market in 2000, it really wasn’t obvious at the time.

Let’s start by looking at the whole bear market, which lasted from March 2000 to March 2003. From this chart it seems obvious that the tech bubble had burst (the green line’s peak), and that it was going to drag the global index into a dark pit:

Past performance is not an indication of future performance. Source: FE Analytics, Total Return 31.12.1999 to 31.12.2003.

It also seems obvious that, at some point in the first half of 2000, you should have abandoned your tech holdings and piled into commodities. Yet clearly it wasn’t, or everyone would have done that. And basically no one did. Why?

Because, while a megatrend shifts from ‘working’ to ‘not working’, confusion reigns. They don’t collapse in a straight line; there are relief rallies along the way. These reassure investors – falsely – that the receding sell-off was just a blip, and that normal service has been resumed.

Witness markets in 2000. Despite bursting in March, the performance case for tech was still intact as late as September. We humans are irrationally swayed by calendar-year performance, so the fact that tech had rallied back from - at one point - a -10% loss for 2000 to a second peak of +23% meant you still looked smart for backing the consensus trade.

At the same time, what we now know to be the emerging consensus of the next decade – commodities - was down just as much in April as tech, and by September still looked a poor bet against its techy counterparts:

Past performance is not an indication of future performance. Source: FE Analytics, Total Return 31.12.1999 to 31.12.2000 (Numbers are to 04.09.2000).

This, in my experience, is what Stage 8 looks like: The ageing consensus has become highly volatile and there’s been a stomach-wrenching sell-off, but worries are eased by significant rebounds. At the same time, other assets, which hindsight will reveal as future world beaters, don’t necessarily excel early on. It is only later, as we approach Stage 9 (Abandoned), that the old consensus decisively dives, while the new potential winners emerge from the carnage.

To be clear; If this is a change of guard, I’m not saying that commodities will be the big winners of the next megatrend - we don’t know what that will be yet. If history is a guide, we’ll see a period of benign chaos as investors scramble to work this out.

It would be fair here to accuse me of talking my own book. Because I love periods of benign chaos; they suit our diversified, multi-active approach. I had an absolute blast as the Commodity Supercycle collapsed, and though I was yet to manage funds in the early noughties, the internet bubble burst would have favoured our kind of active managers too.

You must, then, take everything I’ve written here with a pinch of salt. But don’t dismiss it too lightly: If I’m right, this could prove a timely moment to review your exposure to American exceptionalism. Like their last two presidents, it’s starting to look a little wobbly.

1 I’m of course referring to the 1997 Australian movie, often confused with Kafka’s book of the same name (to my mind the inferior work).

2 Source: FE Analytics, 23.01.25to 16.05.25. S&P500 and FTSE All-Share Indices, Total Return, in both GBP and USD.

Opinions expressed represent the views of the fund manager at the time of publication, are subject to change, and should not be interpreted as investment advice.

Past performance is not a reliable indicator of future performance.

Important notice: this document has been prepared for professional investors and has been approved as a financial promotion by Downing LLP (“Downing”). Capital is at risk and investors should note that their investments and the income derived from them can fall as well as rise and investors may not get back the full amount invested. Downing does not offer investment or tax advice or make recommendations regarding investments. Downing is a trading name of Downing LLP. Downing LLP is authorised and regulated by the Financial Conduct Authority (Firm Reference No. 545025). Registered in England and Wales (No. OC341575). Registered Office: 10 Lower Thames Street London EC3R 6AF.

.jpeg)

.png)