None of the information provided is investment or tax advice. You should always read the associated risks before deciding whether to invest. These can be found on the product pages as well as in our risks overview. Please confirm you have read the information above.

Downing launches new actively managed liquid alternatives fund aiming to deliver 7% to 10%+ per annum and positive returns in most markets. The new MGTS Downing Active Defined Return Assets Fund (‘Active Defined Returns’, the ‘Fund’), is the first fund from its new Liquid Alternatives team.

The Fund is aimed at institutional investors, Discretionary Fund Managers, IFAs and advised sophisticated individual investors, and will primarily consist of UK Government bonds and large-cap equity index options, which provide significant scalability and strong liquidity. It aims to deliver 7% to 10%+ per annum and positive returns in all markets except for a sustained equity market fall (generally more than 35%), over a period of at least six years.

The Fund is the first to be launched by the new Liquid Alternatives Team established by Downing. Collectively, the team has over 125 years of experience and sector knowledge, and includes Tony Stenning, who held senior roles at BlackRock and most recently was CEO of Atlantic House Group; Russell Catley, founder and also a former CEO of Atlantic House Group; Huw Price, a former Executive Director at Santander Asset Management, and Paul Adams, former Head of Cash Equities and Derivatives Sales, Royal Bank of Canada.

The Fund offers investors a compelling building block for multi-asset portfolios, aiming to add consistent and predictable returns, typically secured with a portfolio of UK Government bonds. The unique proposition includes a hybrid approach of using systematic derivative strategies and active management, combining liquid investments with predictable returns, and an equity like risk profile.

Investment strategy: Maximising the probability of delivering predictable defined returns across the economic cycle.

Systematic Liquid Derivatives: Systematic, derivative strategies optimise the equity risk-return profile. The Fund uses rules-based derivative strategies linked to the most liquid, large-cap global equity indices (i.e. FTSE100, S&P500) with the aim of harvesting well-proven consistent returns across a wide corridor of market conditions.

Strong security: The Fund will hold a high-quality portfolio of assets as secure collateral – typically UK Government bonds.

Active benefits: At times, rules-based, passive derivative strategies can underperform when markets move strongly – this is when specialist active management can add incremental gains by monitoring and monetising positions and applying active risk management.

Key benefits

Increased consistency and predictability of returns: Positive returns in all markets except for a sustained equity market fall of more than 35% over at least six years.

Diversification of risk: The Fund’s risk components are diversified across large, liquid equity indices, observation levels and counterparties. Secured with high-quality assets – typically UK Government bonds.

Active management: Our experienced team will actively manage the Fund and its investments to optimise risk and reward for investors.

Russell Catley, Head of Retail, Liquid Alternatives at Downing, said: “Put simply, we focus your investment risk on the probability of receiving the returns you need, not those you don’t. We target the highest probability of delivering 7% to 10%+ per annum with active management adding material incremental gains. We believe that we are building the next evolution of the proven success of Defined Returns funds

The Downing team isseeing strong demand from clients looking for alternatives to large-cap equity funds which are becoming concentrated in technology stocks, or alternatives to UK equity income funds and illiquid alternatives.”

Tony Stenning, Head of Liquid Alternatives at Downing, said: “The launch of our Active Defined Return Assets Fund is a significant milestone in the ambitious build-out of our new Liquid Alternatives strategies. It is a solution-focused fund that should deliver stable high single or low double-digit returns across a wide spectrum of equity market conditions, except for a persistent multi-year bear market. The Fund is designed to enhance balanced portfolios by providing consistent, predictable returns and is suitable for accumulation or drawdown.

“We aim to deliver a unique combination of proven systematic derivative strategies and specialist active management, and we are doing so at a very compelling fee level, below our closest competitors and in line with active ETFs.”

How the Fund is expected to perform in different markets

In bullish markets: UK Government bonds secure the capital, and the equity index options deliver a predictable 7-10%+ return per annum – giving up some less likely upside.

In neutral markets and normal market corrections: UK Government bonds secure the capital, and the index options deliver a predictable 7-10%+ return per annum.

In a sustained sell-off: if markets fall more than the cover to capital loss and do not recover for six years. Then capital is eroded 1:1 in line with the worst performing index.

The average Cover to Capital Loss is targeted at 35%: the average cover to capital loss represents the average level the Global indices within the Fund could fall before capital is at risk.

Fund key risks

Performance: Capital is at risk. Investors may not get back the full amount invested.

Liquidity: Access to capital is always subject to liquidity.

Counterparty risk: Other parties could default on the contractual obligations.

Fund Structure

UK regulated OEIC fund structure, fully UCITS compliant

Daily dealing, at published NAV

Minimum investment: £100,000

SRRI: 6 out of 7

Depositary: Bank of New York

Authorised corporate Director (‘ACD’): Margetts Fund Management Ltd.

I share-class: SEDOL: BM8J604 / ISIN: GB00BM8J6044

F share-class: SEDOL: BM8J615 / ISIN: GB00BM8J6150

Risk warning: Opinions expressed represent the views of the fund manager at the time of publication, are subject to change, and should not be interpreted as investment advice. Please refer to the latest full Prospectus and KIID before investing; your attention is drawn to the risk, fees and taxation factors contained therein. Please note that past performance is not a reliable indicator of future results. Capital is at risk. Investments and the income derived from them can fall as well as rise and investors may not get back the full amount invested. Investments in this fund should be held for the long term.

Important notice: This document is intended for professional investors and has been approved as a financial promotion in line with Section 21 of the FSMA by Downing LLP (“Downing”). This document is for information only and does not form part of a direct offer or invitation to purchase, subscribe for or dispose of securities and no reliance should be placed on it. Downing does not offer investment or tax advice or make recommendations regarding investments. Downing is a trading name of Downing LLP. Downing LLP is authorised and regulated by the Financial Conduct Authority (Firm Reference No. 545025). Registered in England and Wales (No. OC341575). Registered Office: 10 Lower Thames Street, London EC3R 6AF.

1. Introduction and apologies

“The fox knows many things, but the hedgehog knows one big thing.” Isaiah Berlin, The Hedgehog and the Fox; an essay on Tolstoy’s view of history

I’m often asked; why the fox in ‘Downing Fox’?

The quick answer is that it’s a commitment to staying intelligently diversified. I pinched it from the above quote from Isaiah Berlin, which he in turn lifted from an ancient Greek poem. Foxes have lots of small tricks up their sleeves, it explains, while hedgehogs have one big one. The poet was actually arguing in favour of being a hedgehog – that you should specialise in one big thing, then double down on it. In the hedgehog’s case, this is rolling up into a spiky ball that predators can’t penetrate.

This was probably a better metaphor back on the streets of Ancient Greece, what with truck-flattened hedgehogs being a rarer sight. Because specialism is a double-edged sword. Yes; if you pick the right one big thing, you’ll beat everyone else. But Mother Nature – the ultimate fox – is forever trying new tricks, and she’ll always find a way to confound your one big thing. And when she does? You’re roadkill.

At Downing Fox, we religiously avoid relying on one big thing. We run multi-strategy portfolios, with each strategy a different trick up our sleeve. So, if one of them fails, it doesn’t kill the whole. This is because we have a survive-first, thrive-second philosophy, based on the premise that you should never reverse that order: You can’t thrive if you haven’t survived.

I say this as a prelude to our review of 2025, which was another banner year for hedgehogs, not foxes. We can debate what their one big thing was – AI? Mega caps? Index investing? – but there’s little argument that holding a broad menagerie of ideas, as we do, paled in comparison to squeezing tightly into any one of those megatrends (which many investors did, whether they meant to or not).

An apology

I’ll apologise here because I’m writing this grumpy. I shouldn’t be; things are going well. But we portfolio managers need three things to put a zip in our doodah, otherwise we’re no fun to be around: 1) A decent level of assets to manage; 2) good absolute performance; and 3) good relative performance.

We have two of those, but not all three: Assets under management at Downing Fox are healthy and growing - we’re now managing £346m1 of client money and the pipeline is glugging; absolute performance is decent, with our all-equity fund annualising over 10% since it launched (after charges)2; but relative performance – how we look versus our competitors – is sub-par.

It’s the last one that gets under my skin, even though I know it shouldn’t. Our reasons for underperforming are understandable (though you’ll be the judge of that): I think we’re doing something that’s sensible but different to the herd, and that something happens to be out of favour. It still stings though; I’m a competitive man and I don’t do this job to be below-average.

So, we’ll get into that. Why has our relative performance looked slow? And why do I think it will change (which I do)? Looking at 2025 is a useful way to do that: If you can understand why we made good absolute returns last year, but looked slower than our average peer, you’ll understand why that’s been the case since we launched the Fox Funds (in June 2023).

2. Fox Fund range - performance in 2025

Source: Morningstar, total returns in GBP. 31.12.2024 to 31.12.2025. Past performance is not an indication of future performance.

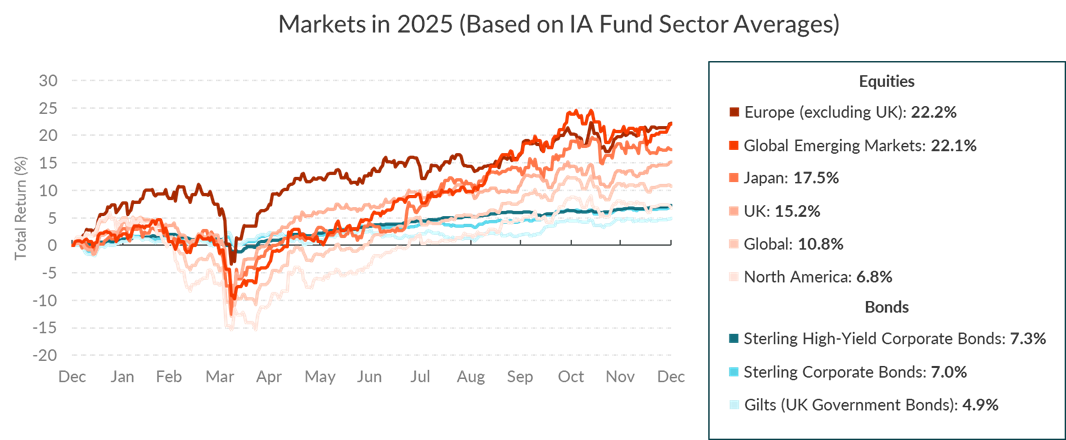

What happened in markets?

That dent you see in the chart above was President Trump’s Liberation Day initiative, which - thanks to the alarming size of that dent – he swiftly abandoned. Other than that, it was a good year for equity markets. The most notable feature was the reversal in fortunes of the US, which dragged its heels (although mostly because of the dollar’s weakness; from a US investor’s perspective, their market’s returns looked a lot higher).

With no notable inflation or interest rate shocks, bond markets had a decent year too. The big winner was gold though, whose price rose by 51%3 in 2025 (in sterling terms).

Our performance vs sectors

The performance of our funds in 2025 is shown below (we’ll add longer-term figures in at the end of this review).

The chart tells the story: In respect of relative performance, our equity portfolio started the year slowly amid the ongoing AI frenzy. It then fared well in the springtime sell-off, which started with Chinese AI stock DeepSeek pooping NVIDIA’s AI party and ended with President Trump’s tariff bombshell. Then, once he’d TACO’d4 out of that, we kept up in a rising market, although this petered out in the summer as the Federal Reserve got speculative juices flowing again with talk of interest rate cuts.

Fox100 ended the year 0.6% behind its benchmark – the IA Global sector average. Disappointing, but far from disastrous5.

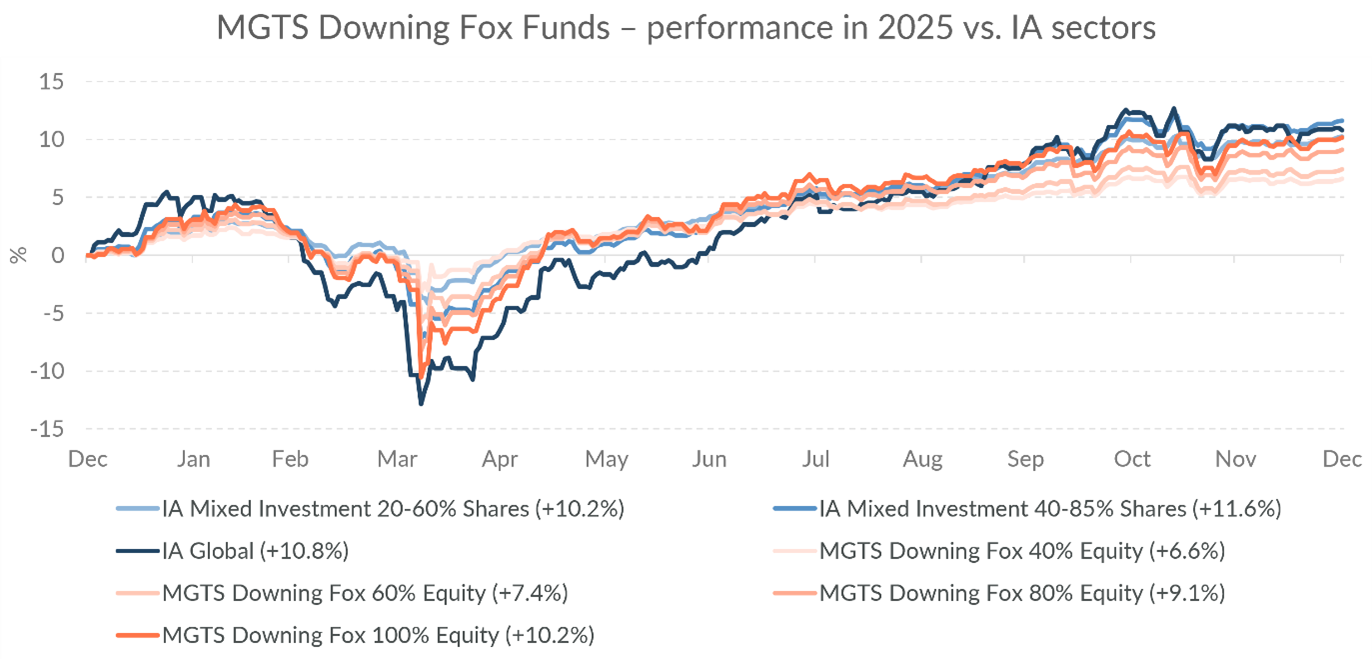

Source: Morningstar, total returns in GBP. 31.12.2024 to 31.12.2025 Past performance is not an indication of future performance.

The gap was wider for the other members of the Fox-Fund family though. Much of this was down to their sectors’ quirks: You know something’s amiss when – in a bumper year for equity market returns - the returns made by the sectors formally known as ‘Cautious’ and ‘Balanced’6 were in the same ballpark as the IA Global sector’s (with ‘Balanced’ actually ahead). The former contains defensive assets as well as equities, while the latter is all-equity, so - in theory – it should make higher returns in a ‘risk on’ year.

Why didn’t it?

Because both of those mixed-investment sectors have greater ‘home bias’. This means they hold more in British equities than you’d find in a global tracker (or in an MP’s pension scheme – miaow!). For years, home bias has been a drag on performance, as it meant holding less in the high-flying US stock market. But not in 2025: The FTSE 100 made 26% last year, dwarfing the S&P 500’s 9%7.

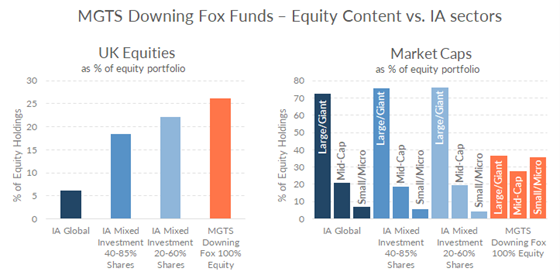

This should have been positive for us, as we also run with a level of home bias. The fact that it wasn’t reveals the key headwind we’ve faced: Two-speed markets, with large-caps motoring while smaller companies trundle behind. Our UK sub-portfolio naturally contains more small and mid-caps than our typical competitor (many of whom use FTSE All-Share trackers for their British exposure), and while Vanguard’s large-cap-heavy UK All-Share Index tracker made 24%, the average UK small-cap fund staggered through the door on New Year’s Eve with a paltry return of just 4%8.

Source: Morningstar as at 31.12.2025

We had other drag factors too, most notably our (permanently) more cautious stance on non-equity holdings. I’ll cover these off in the ‘Growth’ and ‘Defence’ review sections later on.

But to summarise; the big-ticket reason we’re looking slow is our all-active exposure to small and mid- caps (see chart, above). Partly this is because we hold some dedicated small-cap specialist funds, but it’s also because our ‘all-cap’ active managers are finding better opportunities lower down the market too (higher potential returns, lower risk of permanent loss). Our peers, in contrast, are moving away from these assets, replacing them – in many cases – with market-cap-weighted trackers. This naturally gives them a higher weighting to mega-cap companies.

This, to my mind, is where our competitors are hedgehogging: They’re heavily reliant on large- and mega-caps for their performance (their one big thing), so if large-cap fortunes reverse (as they did in the noughties), what have they got?

To be clear, this isn’t a temporary position for us. Downing Fox is hard-wired this way. Partly as a result of our commitment to active equity funds, but also because we think it will lead to higher long-term returns. And, as a further benefit, it gives you a reliable way to diversify your portfolio at a time when more and more products are heavily concentrated in little more than the market’s largest companies.

Finally, as the following chart (from Montanaro Asset Management) suggests, we think small caps are where the best opportunities lie. Mega-caps, in contrast, sit in a range between ‘fine’ and ‘dangerous’. I simply don’t understand why the rush is towards giant companies, when valuations suggest you should be headed in precisely the opposite direction.

What happened within the funds?

As usual we’ll split the rest of the report into two parts: Growth and Defence. We split our mixed-asset Fox Funds into these two components. Growth is responsible for driving the long-term returns of each fund, while Defence is there to make the journey less volatile for those uncomfortable with the ups and downs of an all-equity portfolio (mainly the downs, let’s be frank). This means Fox100 is all Growth, while Fox60 is 60% Growth and 40% Defence.

3. Growth review

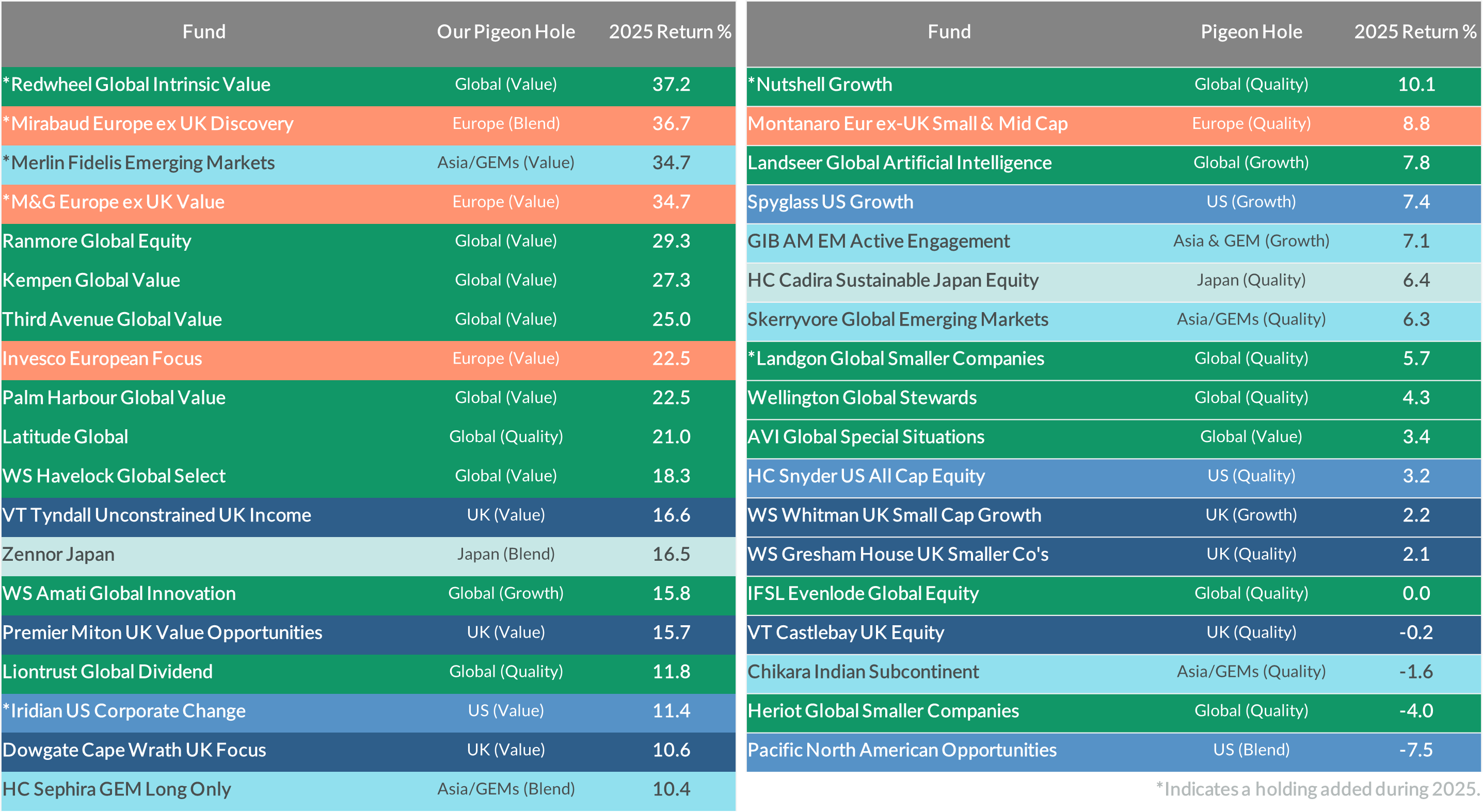

The table overleaf shows how our underlying holdings performed last year. We can’t go through them all, so we’ll pick out a few saints and sinners.

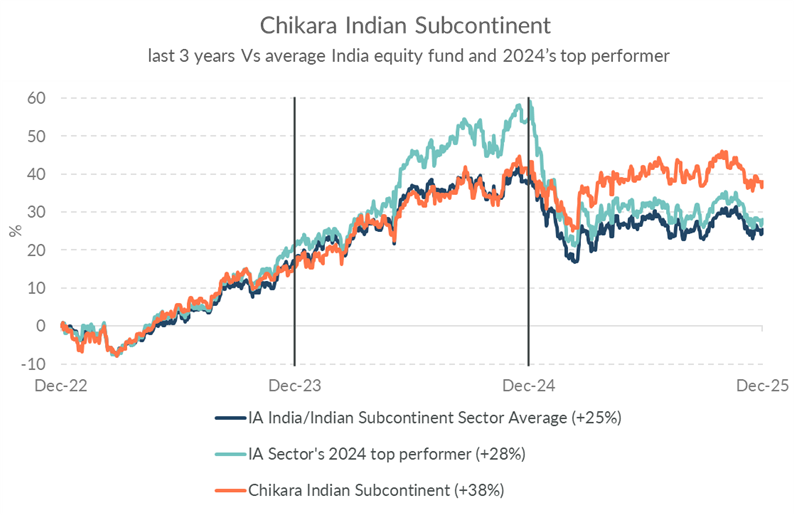

Let’s begin with a fund that sits towards the foot of the table – Chikara Indian Subcontinent. Because in many ways this illustrates what we’re trying to achieve at Downing Fox. It’s a small holding for us, but its loss of 1.6% in a strong year for global equities might make you think this fund is on the sinners list, but the opposite is true: It performed as we would have hoped - we’re chuffed to bits with it.

Source: Morningstar, 31.12.2025. Past performance is not an indication of future performance

Why?

India’s stock market is out of sync with the rest of the world. It’s been through a classic market cycle at the same time that – I theorise – Western markets have been distorted by the impacts of prolonged QE. By ‘classic’ I mean the Indian market rose steeply for a few years, led by its most exciting growth stocks (which tended to be mid and small caps). Whereas Western markets also rose last decade, but they were driven by the kind of big, boring, ‘quality’ stocks that are normally abandoned in the rush for the sexy stuff. Put another way; big and boring is what Western investors found sexy (it takes all types).

Investor excitement meant that, at an index level, Indian stocks looked frothy and over-hyped. But there were enough high-quality companies still trading at reasonable valuations for a talented fund management team to stay invested, and – as long as we hold a fund run by a talented fund management team – enough for us to stay invested too (I think India has a fantastic runway of growth ahead of it; I don’t want to bail out with no good reason).

Last year the air hissed out of India’s market. Some of the funds that had partied hardest in the good times suffered the fiercest hangovers as capital withdrew (the top performing India fund in 2024 lost 18% in 2025). In the face of these losses, Chikara’s minor loss of 1.6% is an outstanding result. It came courtesy of sticking to their process: They focus on high-quality companies, many of which had been ignored in favour of the racy small- and mid-caps. This left them trading at reasonable valuations for what are excellent ways of accessing India’s ongoing growth.

You can see the results on the below chart. As 2025 began, if you’d been judging on performance alone, Chikara’s fund looked average. But when you understood the process, and that the team had been taking significantly less risk than their peers, you could see their keeping up in a rising market was no mean feat. The pay-off then comes when they don’t lose it all as the market sells off.

Source: Morningstar, total returns in GBP. 31.12.2022 to 31.12.2025. Past performance is not an indication of future performance.

I love this performance profile – it’s what I’d realistically like to achieve with the MGTS Downing Fox Funds9. It neatly illustrates the ‘survive-first, thrive-second’ mentality I mentioned before. I’m happy for us to be in the pack as markets rise, but I do expect us to get ahead of peers when they fall. Then, having lost less, we’re in a better position to compound your wealth higher once markets start rising again.

Tough times on Quality Street

Chikara’s performance also illustrates the benefits of the ‘quality’ style of investment. Outside of India, this has had a tough time of it over the last few years, and particularly in 2025 (witness the reversal of fortunes - but not fortune - of ‘quality’ fund manager Terry Smith). A quick glance at our holdings’ performance table shows plenty of funds following this style, and few of them prospered. And if they were small-cap and quality? Ouch – they got hit from two directions.

Naturally this didn’t help our performance, but this is what I promised we’d do: Run great fund managers operating different styles, so that when one style is out, another is in. And if you look to the top of the table, you’ll see many of our ‘value’ funds are making hay while their style shines.

Why, you may ask, don’t you just hold the style that will win that year and avoid the rest?

Because nobody knows which style will win, or for how long. Some of our peers attempt to change horses, but they’re no good at it (many are now out of work – the result of putting thriving ahead of surviving). Indeed, I wasn’t any good at it when I tried it earlier in my career, but thankfully I twigged before I harmed clients’ wealth. Basically, it’s market timing, and nobody’s consistently good at that.

So, despite quality’s travails, we’re not cutting back on this style. In fact, if anything, we’re buying more. This is because the share prices of the high-quality companies beloved by the likes of Mr Smith & Co have fallen far enough to become ‘value’ stocks, and our value managers are starting to add them to their funds too.

In effect this means we’re beginning to double up on quality. And this is very much the Fox way of investing: Whenever a great ‘quality’ manager and a great ‘value’ manager agree on the same stock, you probably should double up on it: It’s likely a great company at a bargain price. This is the hallmark of a good investment. And on a collective basis, I find it reassuring that quality is, once again, underperforming as investors chase the sexy stuff. That’s how it always used to play out before QE, and the resulting cheaper valuations helped quality to shine once the excitement turned to horror.

First and last

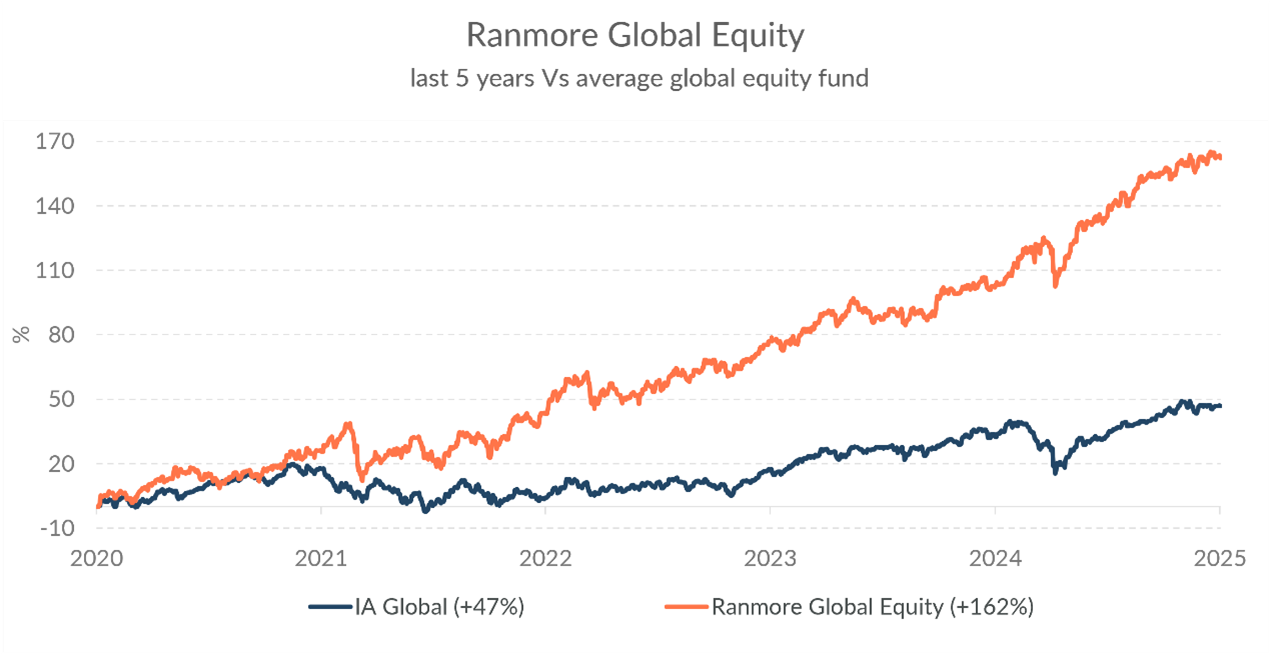

Now we’ll turn to the very top and bottom of the table. We added the top four funds during 2025, so it’s perhaps unfair to focus on them (but we’re happy our continuing efforts to upgrade the portfolio are already bearing fruit). That elevates Ranmore Global Equity to pole position.

This fund, run in the ‘value’ style by Sean Peche, has been a fantastic holding. Here’s its performance over the last five years:

Source: Morningstar, total returns in GBP. 31.12.2019 to 31.12.2025. Past performance is not an indication of future performance.

In other words, its stellar return in 2025 was no flash in the pan. That said, it hasn’t all been plain sailing for Sean. He launched his fund as Terry Smith unveiled Fundsmith (back in 2010), and they’ve followed opposite paths since: While Terry was flourishing amid the quality-friendly decade that followed, Sean’s value style simply didn’t work. Ten years is a long time to run a fund without reward, and it’s to his credit he kept going (many gave up, or were forced to by their c-suites). But since late 2020 (when the good news on COVID vaccines broke) value has started working again, while quality has stopped. Sean’s and Terry’s performance profiles have duly swapped too.

Both, to be clear, are good ways to invest. And as we can’t tell when one style will work and another won’t, we instead choose to ‘cheat’ by holding the best examples of both and pocketing the difference.

At the other end of the table sits Pacific North American Opportunities. While this fund has faced some of the same headwinds mentioned above, it’s added to its own troubles too. When we first bought it in 2023, we had high hopes. Its manager, Chris Fidyk, is a brave investor – he’d sooner poke his own eyes out than buy a stock just to copy a benchmark. We like this in a manager. But the early days of his fund have seen a few swings and misses, and when you swing as hard as Chris has, any miss leaves a mark.

I think he’s learned from the experience and has tempered his approach. We support this, but it’s clear he wasn’t the finished article we expected him to be. So, as much we hope he’s beyond his teething problems, we’ve reduced our position size to reflect the uncertainty. We continue to watch closely.

Activity in 2025

We’re not always that patient with funds: We sold out of ten of them in 2025. The reasons varied, but for the most part it was simply because we thought we’d found a better option, so we took the opportunity to upgrade the quality of our fund manager stable.

There were some exceptions though. We sold First Eagle US Small Cap Opportunities because we felt they’d reneged on our fee arrangement. We operate on trust with our managers, and any breach of that trust is an instant red card.

Then there was Schroders, who removed the managers of the Schroder Emerging Market Value Fund for the apparent crime of them performing too damned well. We immediately sold it (in October), at which point the fund was sat on a 2025 return of 33%10 and was – in my opinion – well on the way to becoming a category-killing best seller. It was a decision as bizarre as it was infuriating. Safe to say we’re unlikely to buy another Schroders fund anytime soon.

On the other side of the roster, we added seven new funds. With each, the bar for inclusion in the Fox portfolio got a little higher. We will keep pushing it upwards.

4. Defence review

It’s tempting to say that the Defence Component performed boringly in a risk-on year and - because it’s paid to do that11 - that’s our review done and we can all go home early. But there’s more to it than that; not least explaining why its 2025 return was lower than you’d have got from cash.

It’s important to understand what this part of Downing Fox is really aiming to do. Because there’s a ‘behavioural investing’ reason for the Defence Component’s existence: Its job is to help risk-averse investors hold at least some exposure to the Growth Component (which is the engine that should drive the majority of the long-term returns made by the Fox Funds).

Clearly the part of investing nervous investors hate isn’t the market heading upwards. It’s not even when share prices drop by a couple of percent (which happens all the time). No, it’s the brutal sell-offs; be they deep and sharp; or shallow but prolonged. In these periods, Defence must dilute Growth’s falling share prices.

Cash is certainly one way of doing that, and a reliable way too: it will stand still while equity markets are falling. What could be better than that?

Something going up while equity markets are falling. This is what the pointy heads call ‘negative correlation’, and it’s something us multi-asset portfolio managers spend a lot of time thinking about. It is, frustratingly, more art than science. Not least because people don’t really want negative correlation, what we really want are things that are negatively correlated when equities are falling (i.e. they’re rising), but then positively correlated when equities are rallying (i.e. they’re still rising). It’s classic cake-and-eat-it territory, because - unsurprisingly - there is no holy grail asset that will automatically do this.

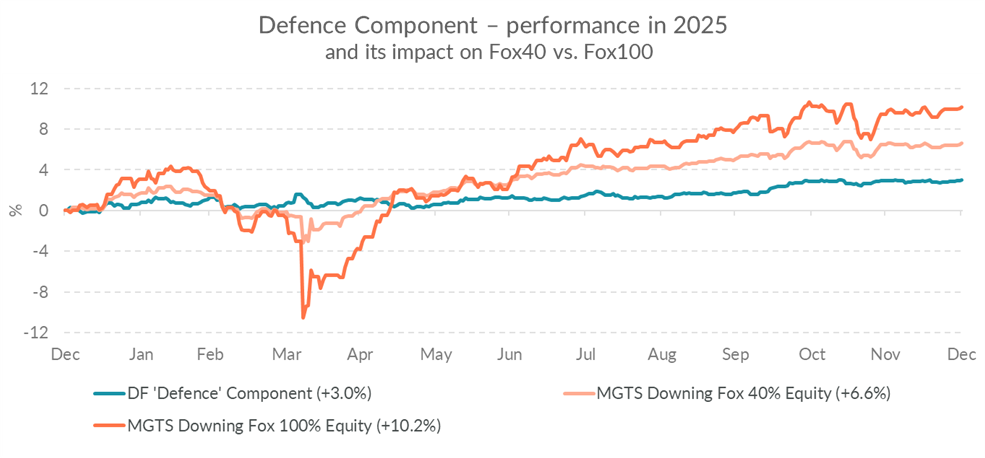

You can see a little example on the chart below of the Growth and Defence models’ performance last year. That modest bump up in the blue line as markets slumped in April is negative correlation, and it helped to make Fox40’s fall not just smaller than Fox100’s, but also smaller than it would have been if we’d used cash instead of the Defence Component. A smoother ride, in other words, helping the twitchier fund holder to keep calm and carry on investing.

Source: Morningstar, total returns in GBP. 31.12.2024 to 31.12.2025. DF ‘Defence Component’ data is based on a simulated model within the Downing Fox model portfolio. Simulated and actual past performance are not indications of future performance.

Obviously, we’d have liked the bump in the blue line to have been bigger, just as we’d have liked its end point on the chart to be higher too. But that’s often the trade-off: Negatively correlated assets can be like a home insurance policy; there’s a cost for holding it, and it only pays out after an event you’d have preferred not to happen. We are, like any buyer of insurance, trying to find the best cover at the cheapest price. If we do this well, the Defence Component will outpace cash over the longer term and bump upwards in the bad times. But, as a predominantly artistic endeavour, there are no guarantees.

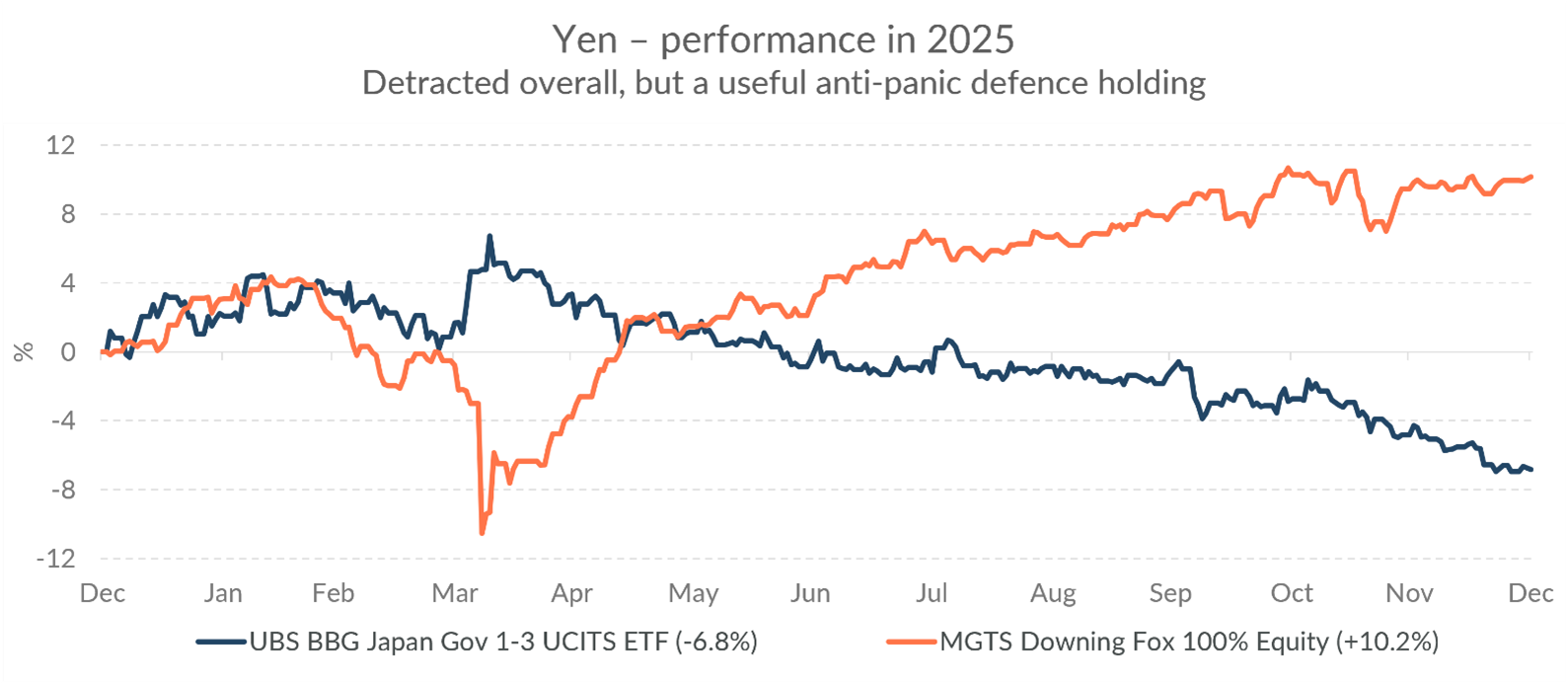

Currently, one of our negatively correlated assets of choice is the Japanese yen. You can see here, via our holding in the UBS ETF, how it performed last year. Like home insurance, it ended up costing us in a good year, but it helped performance in the one period when your clients might have panicked: the Liberation Day sell-off in April. If they had panicked out then, they’d have missed the recovery and subsequent rally. This is one of the acts of self-sabotage that repeatedly hurts retail investors. But looking purely at the one-year return, its inclusion in our Defence Component was a significant reason for it lagging cash in 2025.

Source: Morningstar, total returns in GBP. 31.12.2024 to 31.12.2025. Past performance is not an indication of future performance.

It’s important to note that negative correlation itself isn’t enough to justify holding it. The yen’s overall performance last year was disappointing. Ideally, we’ll find assets that give us the same emergency bump and provide a return that competes with cash. What gives us extra reason to hold yen right now is that it currently looks cheap. There are technical ways of valuing currencies, but that the cost of sushi for four has dropped enough for me to finally consider a family trip to Tokyo speaks volumes.

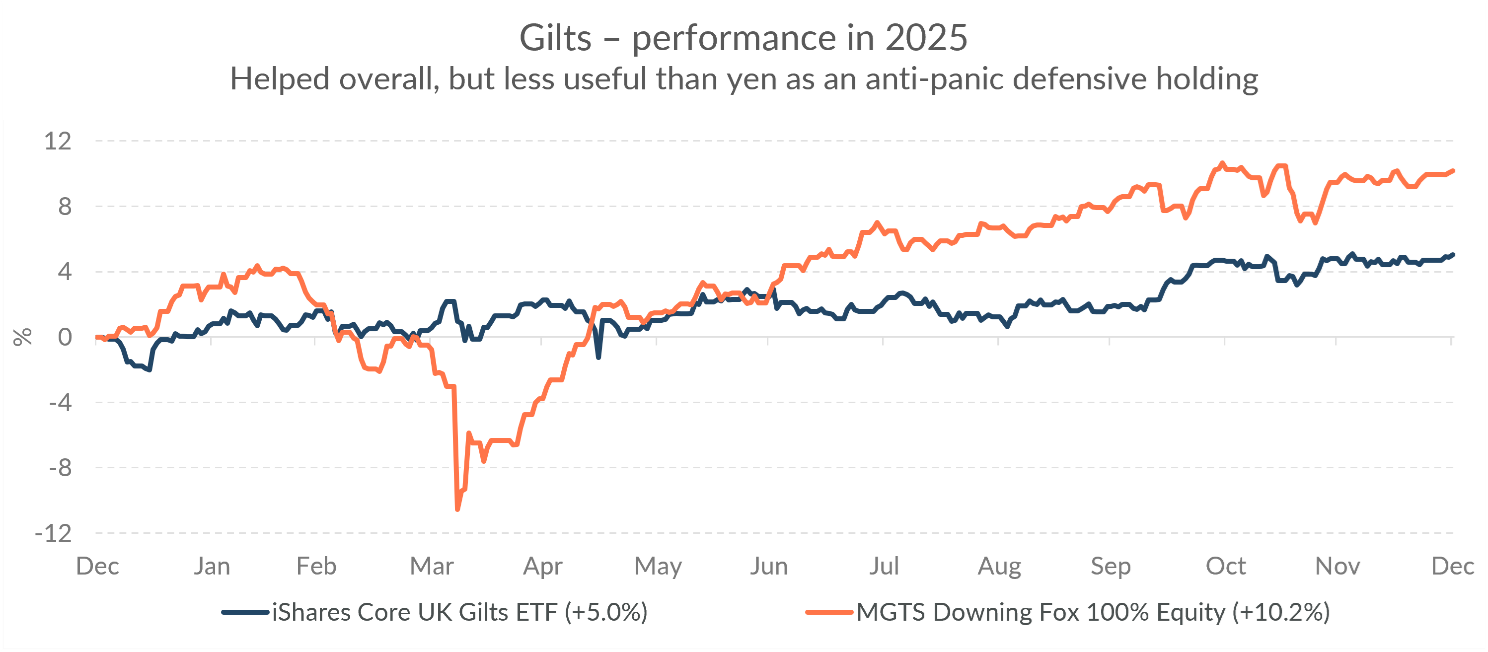

Thankfully our holdings in gilts fared better last year. As the chart shows, they gave us some insurance payout in April, albeit less than the yen’s, but they did give us a better year-end result:

Source: Morningstar, total returns in GBP. 31.12.2024 to 31.12.2025. Past performance is not an indication of future performance.

Why not go all gilts then?

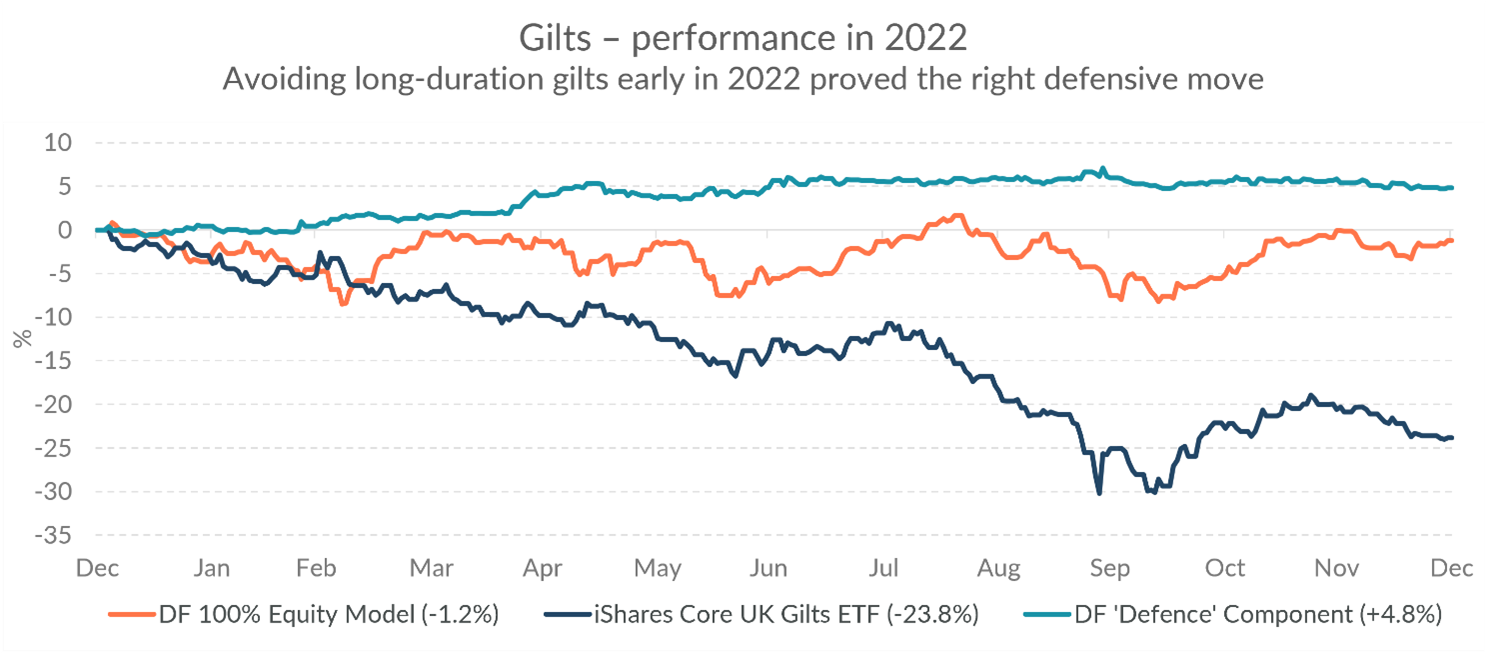

The rub is, there’s no guarantee that any one defensive choice will pay out. If it’s the wrong type of sell-off for that particular asset, it could actually make the experience worse, which is what happened to any hedgehogs relying on gilts as their one big defensive thing in 2022 (see chart). This is another way in which we’re in Camp Fox – we prefer to use many tricks, not just one, to achieve our defensive ends.

Source: Morningstar, total returns in GBP. 31.12.2021 to 31.12.2022. DF 100% Equity and DF Defence Component data is based on simulated models. Simulated and actual past performance is not an indication of future performance.

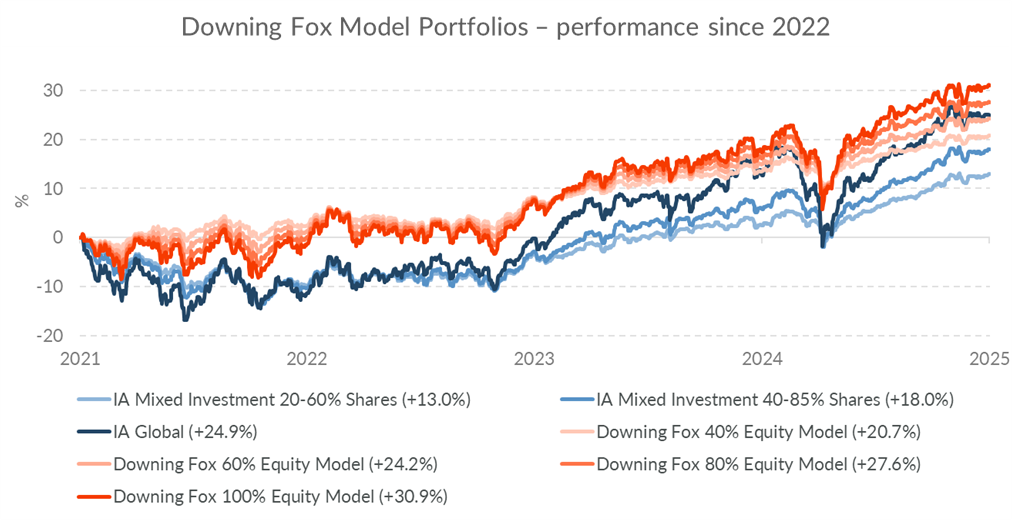

5. Longer-term performance

For context, here are our longer-term returns. Starting off with the performance of our model portfolios, which date back the furthest (to the beginning of 2022, just before I officially joined Downing). These were the models into which our clients’ money was first invested via the white-labelled funds we’ve been advising since 1 April 202212. Hopefully you can see how, over this longer timeframe, we’re delivering what I want: Keeping up in the good times, and holding up better when it all hits the fan:

Source: Morningstar, total returns in GBP. 31.12.2021 to 31.12.2025. Downing Fox data are simulated models. Simulated and actual past performance are not an indication of future performance.

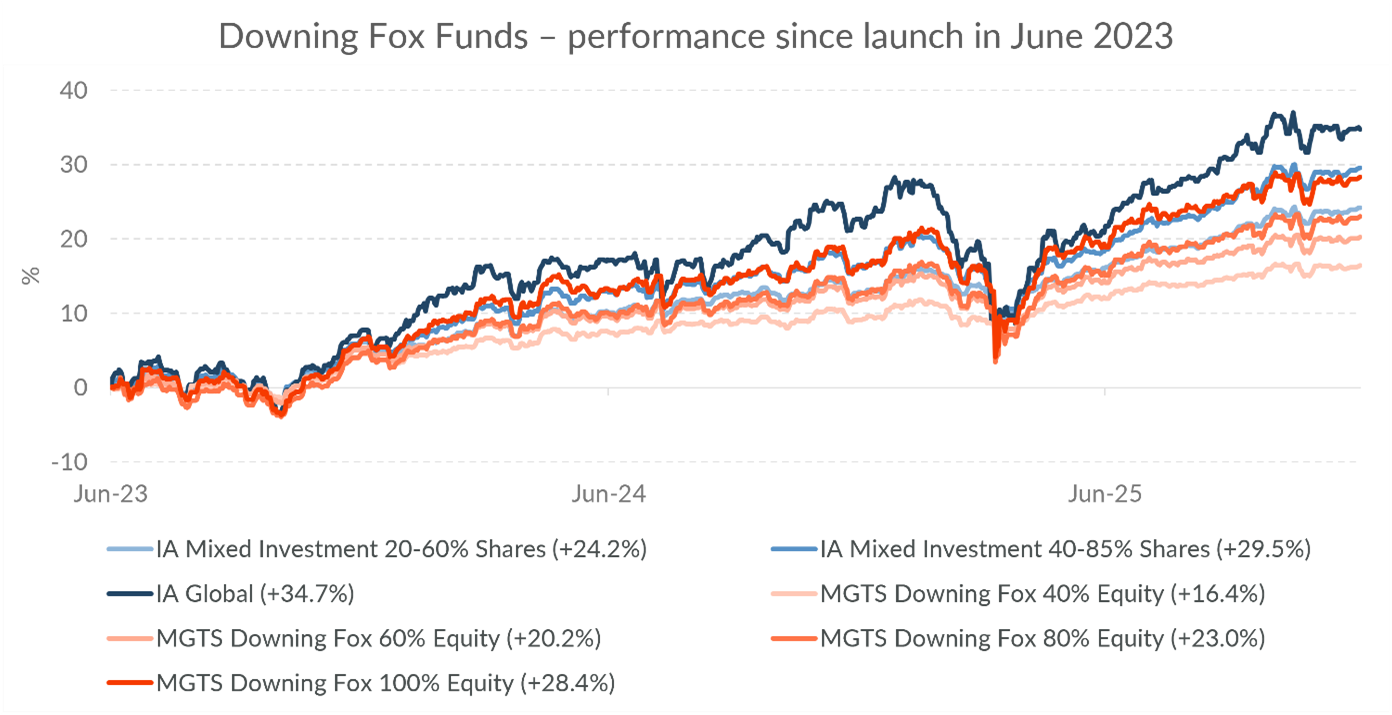

Our Fox Funds were finally launched in June 2023, by which time the beleaguered assets our competitors held in 2022 - that we hadn’t - had started to bounce back. We had also moved into the AI frenzy (kicked off by the launch of ChatGPT in November 2022) and mega-cap dominance, neither of which are fox-friendly trends:

Source: Morningstar, total returns in GBP. 27.06.2023 to 31.12.2025. Simulated and actual past performance are not an indication of future performance.

Had I known markets would play this trick on us, I might have lost the ‘Fox’ and called us Downing Tortoise instead.

6. Outlook?

That question mark in the subtitle is a permanent feature: Should we even provide an ‘outlook’, it asks, when we think forecasting is a dangerous waste of time? Probably not. But it feels like the done thing, so I’ll try to thread the needle.

The big picture

In terms of ‘the macro’, I’m sure I’m in the same boat as you: the world feels like an increasingly scary place. But everyone feels that way, so current scariness may be ‘priced in’. It’s also been scary before, and what we can’t know is when ‘peak scary’ will be. We might even be past it already. I certainly hope so. Naturally I have personal views on this, but I keep them out of the funds, so I’ll keep them out of this review too. You’ll have to take me out for a beer to hear them.

What I can talk about here are valuations. These can tell you something about what long-term returns we might expect (but sadly nothing about market timing). From a global market perspective, future returns look likely to be weak. But my negativity is due to how much the global market is dominated by mega caps, particularly American ones. These look uncomfortably expensive at a time when almost everything else looks somewhere between OK and attractive.

And ‘almost everywhere else’ is a pretty good way of describing our positioning. My own investable wealth remains in the Fox Funds (most of that is in Fox100). I haven’t sold anything either, and will - if anything - add more this year. Given our avoidance of the overvalued stuff, I see no reason not to.

To end, I’ve copied a paragraph from my Outlook? section last year. I’m proud (but not pleased) to say this is one forecast I got exactly right. So, in the interests of sustainability, I’ve recycled it here by scribbling out ‘2025’ and replacing it with ‘2026’:

“My one prediction for 2025 2026 then, is much the same as my prediction for 2024: If the world’s largest companies continue to be the best performers, we will look unexceptional at best. But if they underperform, as they did in 2022, we’re likely to have a better year than our peer groups.”

That’s all. If you have questions, you know where we are. Thank you for your interest and support.

Sign up to the Fox mailing list to receive helpful insights on trends, markets and performance.

References

1 Source: Downing as at 20.01.2026 (AUM consisting of MGTS Downing Fox Funds & mandates managed under the same strategy). 2 Source: FE Fundinfo. The MGTS Downing Fox 100% Equity A Shares have returned 10.3% annualised from 27.06.2023. (launch) to 31.12.2025 against the IA Global TR Index which returned 12.7%. Past performance is not a reliable indicator of future returns. 3 Source: FE Fundinfo, 31.12.2024 to 31.12.2025. 4 TACO (Trump Always Chickens Out) became the go-to acronym for a while back in 2025. 5 When we account for the technicality of the one-day pricing delay on our fund of funds (yawn), we actually beat the sector average by 0.8%. But this seems churlish to bring up in the letter, so I’m griping about it in a footnote instead. 6 These sectors are now officially known as the IA 20-60% Shares Mixed Investment Sector and the IA 40-85% Shares Mixed Investment sectors. I completely understand why the IA changed their names, but I like to keep an investment letter zinging along, and on this basis the wordy new names are a total attention killer. 7 Source: FE Fundinfo: FTSE 100 TR in GB terms was 25.8%, the S&P 500 TR in GB terms was 9.3%. 31.12.2024 to 31.12.2025. 8 Source: FE Fundinfo: 31.12.2024 to 31.12.2025. 9 Unrealistically I’d like them to shoot the lights out in rising markets then stay flat in falling markets. 10 Source: FE Fundinfo, 31.12.2024 to 01.10.2025 11 We give away the part of each Fox Fund that’s invested in the Defence Component for free, so strictly speaking that’s what it’s *not* paid to do. 12 The VT Johnston Cautious Portfolio Fund is run on the Fox40 model, and the VT Johnston Growth Portfolio is run on the Fox80 model.

Opinions expressed represent the views of the fund manager at the time of publication, are subject to change, and should not be interpreted as investment advice.

Important notice: this document has been prepared for professional investors and has been approved as a financial promotion by Downing LLP (“Downing”). Capital is at risk and investors should note that their investments and the income derived from them can fall as well as rise and investors may not get back the full amount invested. Downing is a trading name of Downing LLP. Downing LLP is authorised and regulated by the Financial Conduct Authority (Firm Reference No. 545025). Registered in England and Wales (No. OC341575). Registered Office: 10 Lower Thames Street London EC3R 6AF.

.jpeg)

.png)